Ratio Trading the Earnings

Ratio trading is a well-known strategy among traders. It can take various forms, but one popular method is the Hedged Straddle. This involves offsetting a larger number of long positions with short positions that are closer in time. Essentially, it’s a more sophisticated version of the basic strategy of selling one short ITM (In The Money) option while buying two long ITM options, often resulting in zero cash outlay or a minor cash flow adjustment, aside from margin requirements.

This article reflects my thoughts on using this option strategy, inspired by what I’ve learned here on SteadyOptions. I welcome your feedback—agree or disagree, I look forward to the discussion. The classic trade works for both calls and puts, but for illustrative purposes, I will focus on calls.

You might wonder why one would consider a ratio trade ahead of earnings announcements.

- Many stocks tend to increase in price before earnings announcements.

- As noted in the SO long calendar, implied volatility (IV) typically rises before earnings. ITM options are less affected by rising IV compared to ATM or OTM options, making this trade beneficial.

- Black swan protection: If the market experiences a significant downturn, the stock may end up below the short strike (if calls), resulting in a safe wash for the entire trade.

In simpler terms, a ratio trade before earnings allows you to participate in the market without risking substantial losses. If managed well, your losses can be mitigated. Those who have purchased long calls before earnings know the thrill of a 100%+ rise, but also the disappointment of losing everything when the market moves against them. While a straightforward long position can be rewarding if you’re right about the direction, a ratio trade enables you to attempt this multiple times without significant risk.

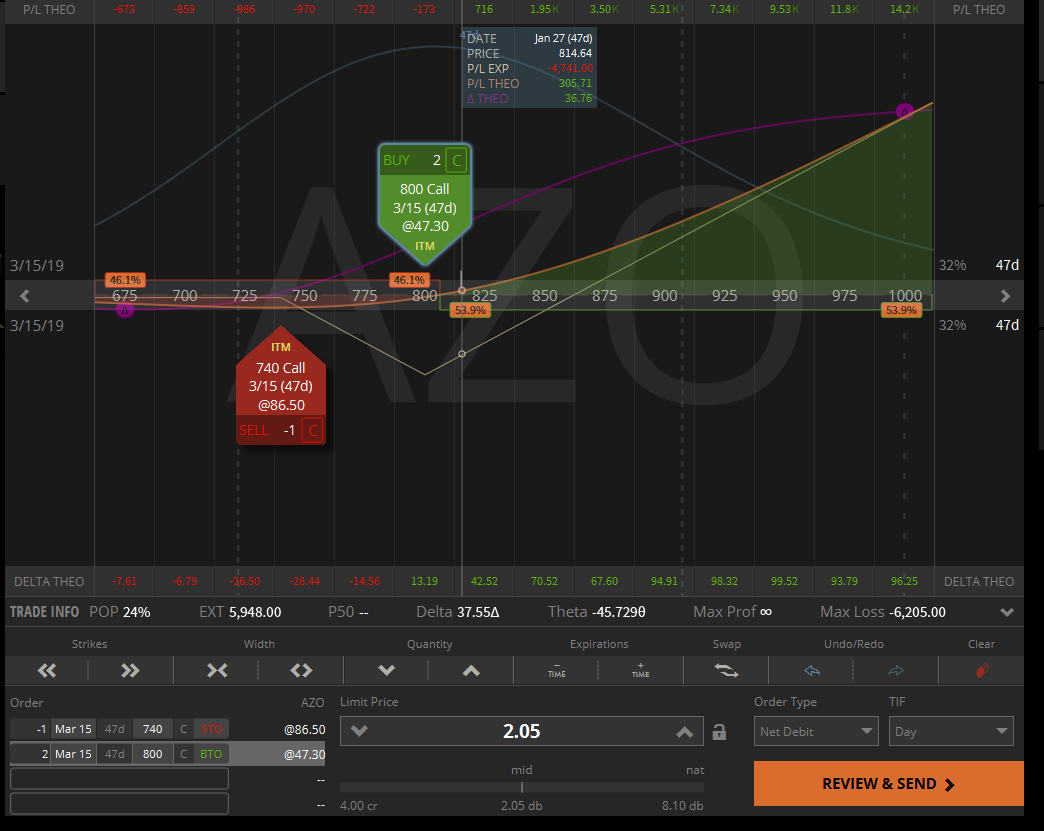

Some may be skeptical about the impact of IV, but it can be significant. For example, consider AZO, a stock that often rises before earnings. While it may not be the perfect example due to its high stock price and margin requirements, it serves as a real-world illustration. In any earnings week, there are usually several potential candidates. Below is a schematic of an AZO 1:2 ratio based on 80 (short) and 60 (long) delta calls for March 15 (post-earnings).

I anticipate that the IV of this position will rise to 112% the day before earnings. If I input that IV today, the position would gain $10K immediately.

Even if the stock remains unchanged, our position would theoretically gain value under these parameters. While reality can be unpredictable, the effect of rising IV serves as a buffer against theta losses, and we could profit significantly if the stock moves favorably.

What Do I Need to Choose My Trade?

When selecting a stock for trading, consider the following questions:

- Does this stock typically rise before earnings?

- When should I enter and exit the position?

- What are the ideal deltas for the short and long positions to maximize profits?

- What ratio should I use?

- What will the IV be at the planned end time of my trade?

- What stock price would allow me to break even at the planned exit date, and what price would achieve my target profit?

Answering these questions allows for a structured trading plan. If everything looks favorable on the day, execute the plan and use it as a guideline for taking profits or cutting losses. Let’s explore these questions using tools commonly utilized by traders on SO. While some tools may require payment, they are often worth the investment. With some effort, you can achieve similar results using charting software.

Which Stocks Rise Before Earnings?

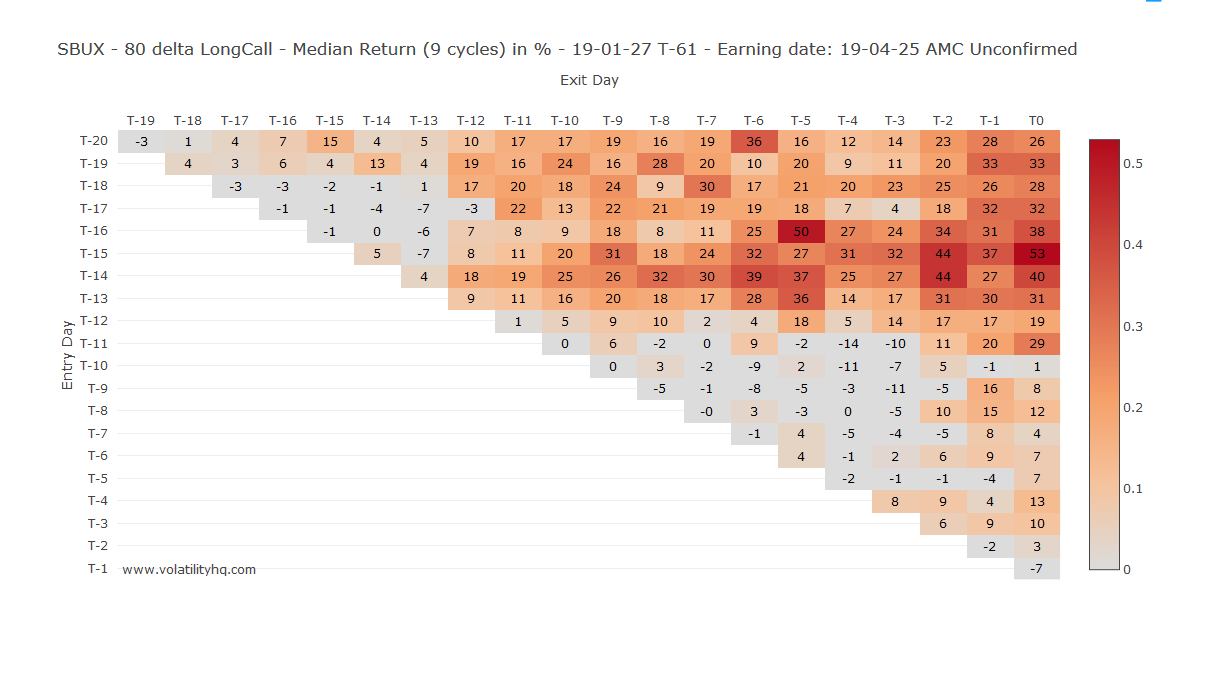

You could manually check stocks and their previous earnings dates, but I’ve found VolHQ’s return scanner matrix to be incredibly useful. For example, SBUX has consistently performed well. Here’s a heat map illustrating this:

This heat map shows substantial profit opportunities. I typically start with the 80D option, as it closely aligns with the actual stock value. Conversely, UAA is not a good candidate for this strategy, although it may be suitable for a ratio put trade.

When Should I Enter and Exit the Position?

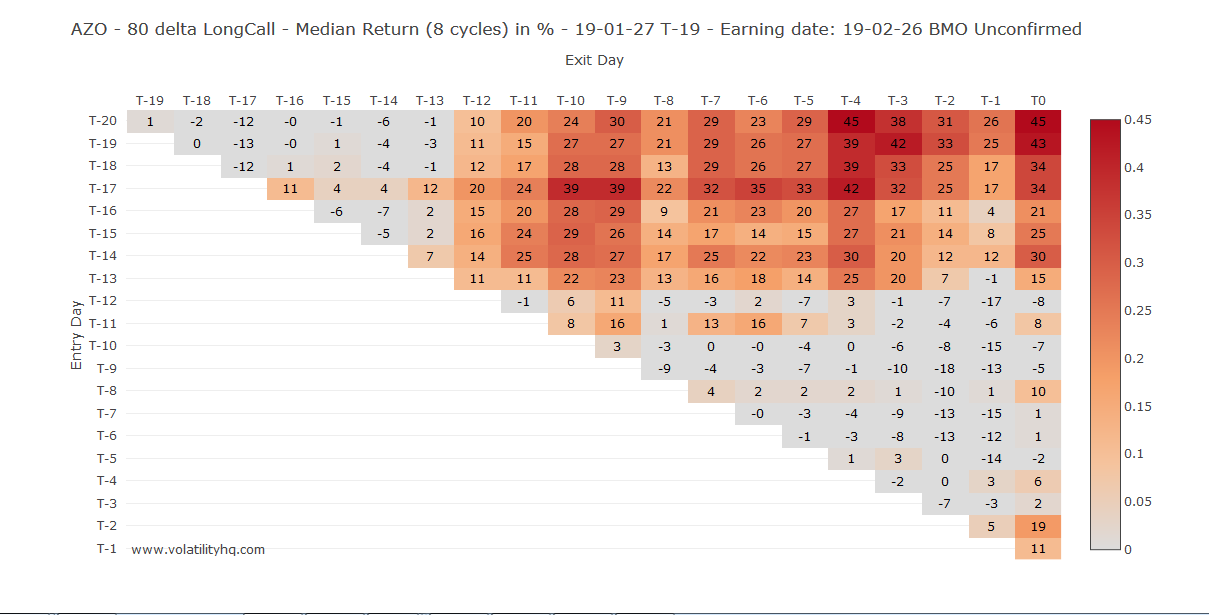

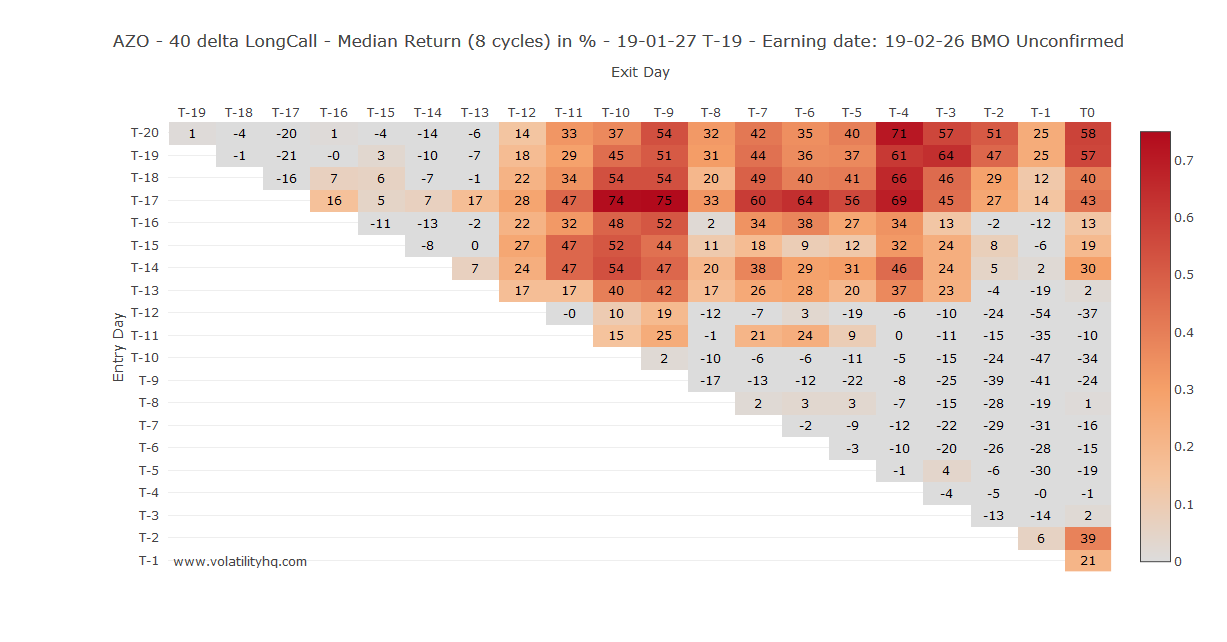

Referring back to AZO, the 80 Delta Return matrix looks promising:

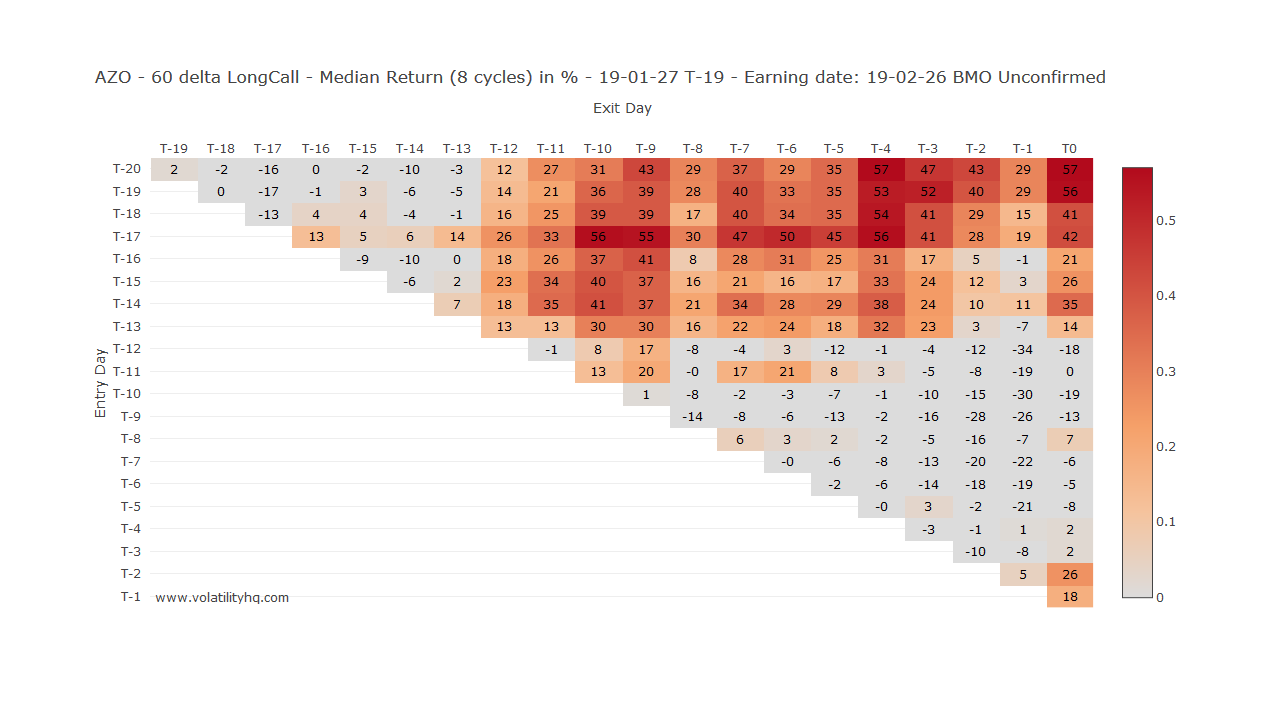

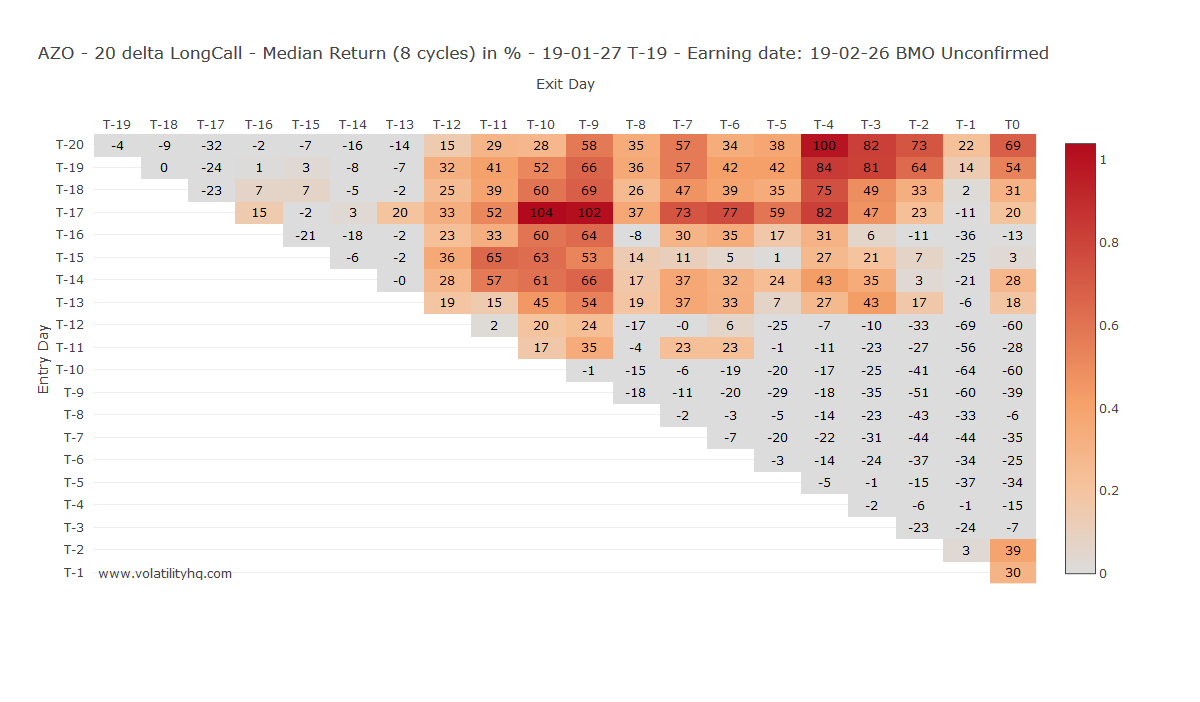

We should also check the 60, 40, and 20 D long call returns:

Observing the heat map, it appears that the most consistent opportunities lie between T-20/T-16 for opening and T-12/T-8 for closing. The highest returns seem to occur around T-17 for opening and T-9 for closing, allowing time to adapt before earnings are announced. Therefore, we should aim to open the trade around February 8 and close it by February 18.

What Are the Ideal Deltas for the Options Used in the Ratio?

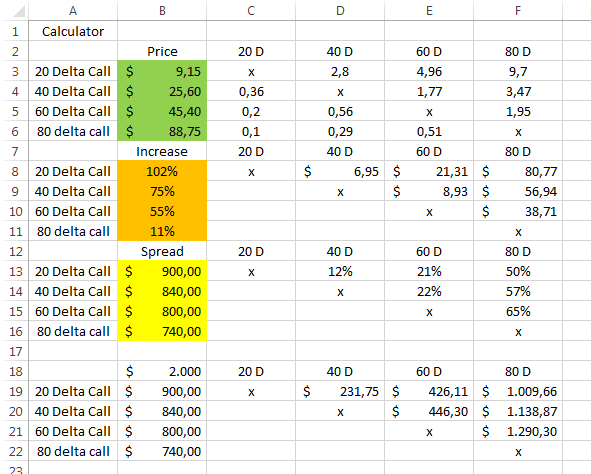

Initially, I believed that a one-strike ITM and one-strike OTM approach was optimal, or that a 1:3 ratio was necessary. However, the ideal ratio depends on the stock, IV, and timing. There are no hard and fast rules, but higher delta ratios tend to be more effective. This calculation can be complex, as it requires comparing like-for-like options while considering margin differences and other pricing parameters. I created a spreadsheet to facilitate this analysis.

You need to determine the stock price corresponding to the 80/60/40/20 delta calls for the option series ending soon after the earnings announcement. In this case, I chose the regular 3rd Friday expiry for liquidity and relevance. The relevant strike prices are not exactly aligned but are close enough for my analysis.

The orange section of my spreadsheet shows the return based on the VolatilityHQ return matrix, while the green section reflects last Friday’s mid-price of the options. To identify the ideal delta combination, we examine the third and fourth sets of tables marked SPREAD and $2000, which provide returns in percentage and based on a hypothetical $2000 investment, respectively. In this case, the 80 delta short and 60 delta long appears to yield the highest return of 65%.

What Ratio Should I Use?

My spreadsheet indicates that a 2:1 ratio is appropriate when matching the 60 DELTA Call against the 80 Delta call.

Great, you might think, but can I trade now?

Not yet. There are several more considerations before executing the trade.

What Will the IV Be at the End of the Trade?

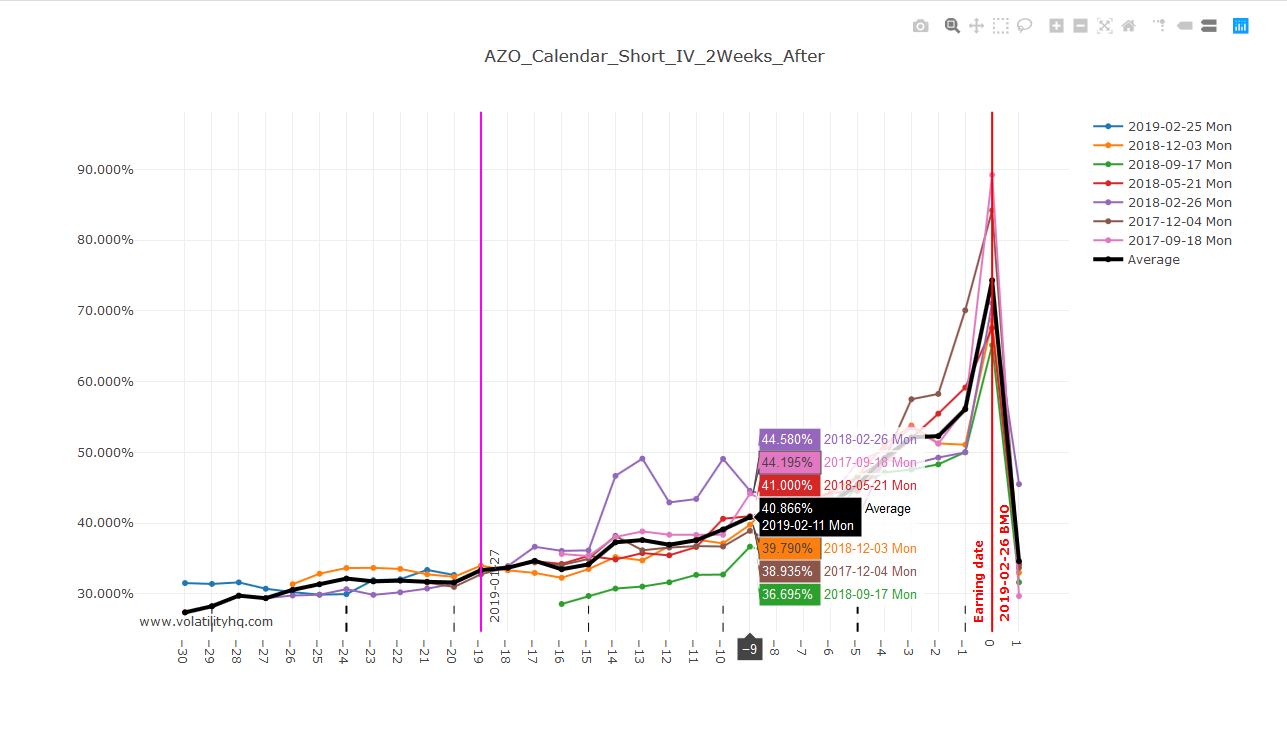

I return to VolatilityHQ to check the normal calendar function. This is useful for assessing whether the stock is suitable for a calendar trade. The third chart down on the calendar plots from VolHQ provides valuable insights.

By T-9, our proposed exit date for the trade, IV would be around 41%. We can now input this into our option valuation, as we have entry prices and know our exit date and IV at that time.

What Is My Breakeven/Target Profit Stock Price at Exit Day?

Our breakeven price is today’s stock price, which is reassuring. Even if nothing happens, we should be relatively safe. The projection for the exit date at T-9 indicates:

For our profit target, let’s aim for 50%. It’s wise to be conservative and take profits when available. This would yield a profit of around $3K, given a margin requirement of over $6K. This target is approximately $871.50 for AZO, which is only a 7% increase from today’s price—well within the range of previous earnings run-ups.

We Have a Plan:

- Enter the trade on February 8 with a 2:1 ratio of the 740/800$ 15-Mar call options.

- Exit by February 18 at the latest.

- If the stock hits $870+, liquidate, as this would be our target exit.

- If the option threatens to drop below $814, consider cutting losses. The large cushion of IV makes this less problematic.

Potential Issues (Caveats)

What are the downsides and tricky aspects of this trade?

- The black swan protection may provide a false sense of security. Many believe the trade will be safe if the stock tanks, but it must NOT be held through earnings. Elevated IV can lead to options being priced well below their value post-earnings, resulting in significant losses.

- Finding the right stock is challenging. The heatmaps on VolHQ are averages, so it’s crucial to hover over the entry and exit date crossings to see the actual averages.

- Liquidity is vital; avoid stocks with wide spreads. While the ratio is more forgiving than a calendar, you still need to manage spreads effectively.

- You must repeat your prep work before committing to the trade, as parameters may change in the interim.

- Monitor these trades closely and verify actual earnings dates. Even consistent past performance is no guarantee, and holding through earnings can lead to significant losses.

Any Soothing Words?

No system is perfect, and I welcome your feedback. My experience has been positive, especially as I’ve refined my approach to selecting ratios for each stock. My batting ratio includes:

- Profitable on target (or near enough, always more than 10% on average 18%): 26

- Around 0% (includes +5/-5% but mostly just +1/-1%): 18

- Losers averaging about -20%: 10

Since refining my delta selection, my hit ratio has improved, with minimal losses. I typically trade blocks of $2-3K, occasionally exceeding $6K. This strategy is suitable for retail investors, as institutional traders often face worse prices due to their volume.

Would you like to learn in real-time how to identify these opportunities and trade them? Click the button below to get started!

Related articles: