Energy companies often face unpredictability, with their results fluctuating based on oil prices. However, certain players manage to distinguish themselves through discipline, scale, and consistent shareholder rewards. One such example is a global powerhouse that adeptly balances production with refining, transforming barrels into reliable cash flow.

A Business Built for Energy Cycles

Chevron Corporation (CVX) stands as one of the largest integrated oil and gas companies globally, ranking as the second-largest U.S. energy major after ExxonMobil. Its operations are divided into two main segments:

-

Upstream (≈75% of earnings in recent years): This segment focuses on the exploration, development, and production of crude oil and natural gas, including liquefied natural gas (LNG). Chevron boasts a dominant position in the Permian Basin, long-life production in Kazakhstan’s Tengizchevroil, and increasing volumes from the Gulf of Mexico. The company also holds stakes in significant international pipelines and engages in carbon capture and storage initiatives.

-

Downstream (≈25% of earnings): This segment involves refining crude oil into fuels, lubricants, petrochemicals, and additives. It also encompasses the marketing of refined products, pipeline operations, and a growing portfolio of renewable fuels. Chevron operates approximately 1.8 million barrels per day of refining capacity worldwide.

Chevron’s vertical integration allows it to generate profits at various stages of the value chain. High oil prices enhance upstream earnings, while refining and marketing activities can mitigate downturn impacts. This balance, along with disciplined capital allocation, supports Chevron’s ability to consistently return cash to shareholders through dividends and buybacks.

When Oil Majors Play It Smart

Bull Case: A Machine for Free Cash Flow

The integration of Hess has proven to be a strategic move, with $1 billion in synergies anticipated this year. Management has raised 2026 free cash flow guidance to $12.5 billion, signaling that dividends and buybacks take precedence over growth. This acquisition also secures long-term growth from Guyana, one of the world’s most promising oil basins.

Chevron’s low-cost upstream barrels are another advantage. Over 70% of its production consists of liquids, which historically yield stronger cash margins. The Permian acreage benefits from unusually low royalty rates, providing a cost edge over competitors. Coupled with disciplined capital allocation, Chevron can continue generating cash even if oil prices remain stagnant.

Production growth is on track, with significant contributions from Tengiz and Gulf of Mexico projects. Management aims for 6–8% growth in 2025, moderating in 2026 to maintain discipline. This approach exemplifies the “slow and steady wins the race” philosophy, which is crucial for dividend investors.

Bear Case: Still an Oil Game

Despite a strong portfolio, Chevron operates in a commodity-driven environment. A decline in crude oil prices due to oversupply or weak demand can quickly diminish cash flow. The liquids-heavy mix that boosts margins during high prices can lead to earnings volatility during downturns.

Downstream operations have faced challenges, with losses impacting overall results. This poses a risk when refining margins compress, potentially exacerbating downturns rather than balancing them.

While the Permian is profitable, it has high decline rates that necessitate continuous reinvestment. Additional challenges include cost inflation, tariffs, and execution risks in large projects like Tengiz. Investors should also be aware that large-scale energy investments are often susceptible to delays and cost overruns.

Free Webinar: Avoid Price Confusion

When stock prices fluctuate, many investors react impulsively. However, successful investors focus on thoroughly examining the underlying business.

👉 Join our free webinar on Thursday, September 18 at 1:00 p.m. ET:

-

Learn a simple framework to discern when to ignore headlines and when to pay attention

-

Utilize the Dividend Triangle to differentiate bargains from traps

-

Gain a repeatable method to invest with confidence

Seats are limited to the first 500 attendees. Can’t attend live? No worries — a replay will be sent to all registrants.

Save your spot (or get the replay): dividendmonk.com/webinar

What’s New: Output Up, Prices Down

The latest quarter showcased the dual nature of the oil industry:

-

Revenue down 12% and EPS down 31%, impacted by lower commodity prices.

-

Record production of 3.4 million boe/d, including over 1 million boe/d from the Permian.

-

Growth contributions from Tengizchevroil and Gulf of Mexico projects.

-

Ballymore subsea tieback start-up supported volumes.

-

Downstream and chemicals reported mixed margins, offsetting some upstream gains.

In summary, while operations were solid, realizations (prices) led to financial weakness.

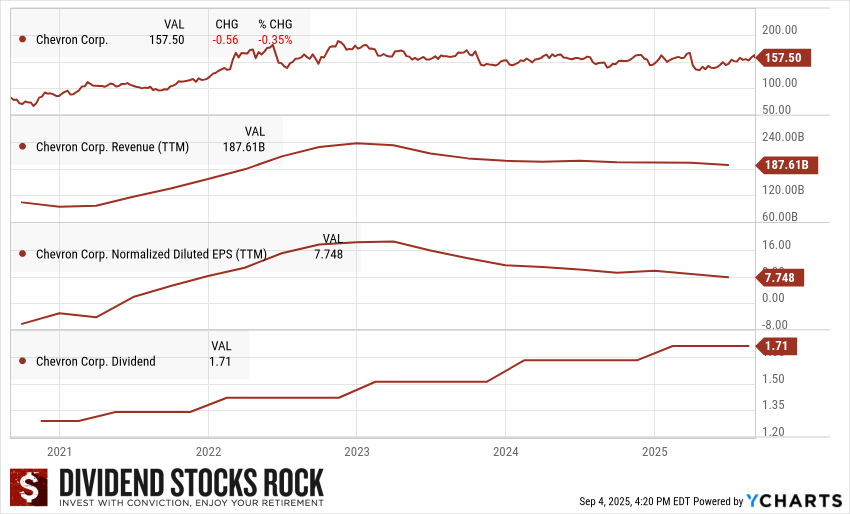

The Dividend Triangle in Motion

Chevron’s Dividend Triangle illustrates a blend of stability and cyclicality:

-

Revenue: With nearly $188 billion, revenue reflects operational strength and the inevitable impact of commodity cycles. Recent years show stability following the post-2022 surge.

-

EPS: Earnings per share remain cyclical, peaking with rising oil prices and compressing during downturns. The latest dip highlights the risks associated with reliance on commodity realizations.

-

Dividend: Currently at $1.71 per share quarterly, the dividend continues its upward trajectory. Supported by strong free cash flow, the dividend’s safety remains intact.

This equilibrium of revenue scale, cyclical EPS, and increasing dividends explains why many investors consider Chevron a core energy investment.