A long straddle options spread represents the buying side of an options straddle strategy. This involves purchasing both a put and a call option with the same strike price and expiration date. As a market-neutral strategy, it offers limited risk with unlimited profit potential, aiming to benefit from increased volatility, regardless of the direction of the underlying asset’s price movement.

Conversely, a short straddle options spread is the selling side of this strategy, designed to capitalize on low volatility when the price of the underlying asset remains close to the straddle’s strike price at expiration.

A long straddle is executed by simultaneously purchasing a put option and a call option at the same strike price and expiration date. This strategy is characterized by limited risk and unlimited profit potential.

A long straddle option strategy is vega positive, gamma positive, and theta negative. It operates on the premise that both call and put options have unlimited profit potential but limited loss. If the stock price remains stable, the straddle option will incur losses daily due to time decay, which accelerates as expiration approaches.

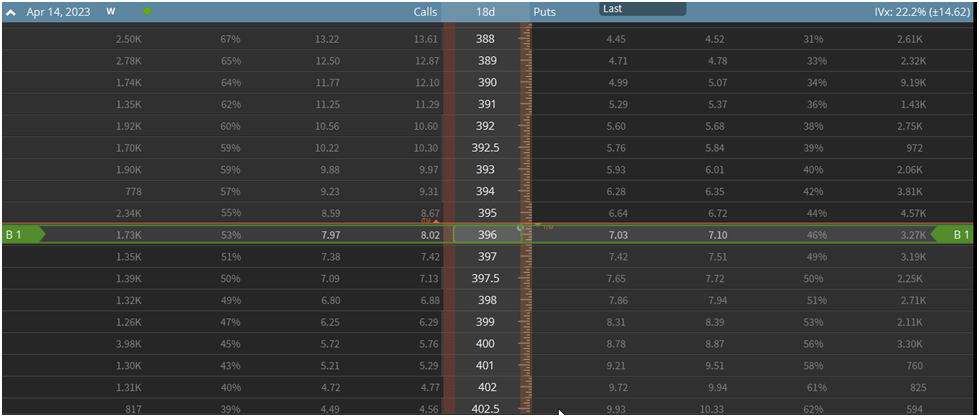

For instance, if the SPDR S&P 500 ETF (SPY) is trading at $396 per share, we might anticipate a significant move in the S&P 500 but remain uncertain about the direction. In this scenario, we could purchase an at-the-money (ATM) straddle, which entails buying both an ATM put and call option.

In this case, we’d buy the following options:

- BUY 1 396 Put @ $8.06

- BUY 1 396 Call @ 9.31

- Total trade cost: $17.37 (net debit)

By purchasing both an at-the-money put and call option, we stand to profit from significant price movements in either direction. However, this strategy comes with a high cost, as evidenced by the substantial premium outlay of $17.37, which represents over 4% of the total underlying stock price. Therefore, a significant move in SPY is necessary for our position to yield a profit.

.thumb.jpg.994f8ab59633ccf69676266a22946b18.jpg)

Characteristics of a Long Straddle Option

The Long Straddle is Market Neutral

A long straddle option is a market-neutral option spread, meaning it does not attempt to predict the future price of the underlying stock. Instead, it aims to profit from significant price movements, regardless of direction.

For example, if we purchase the long straddle on SPY mentioned earlier, if the price of SPY rises significantly, our call option will become profitable, allowing us to sell it for a profit. Conversely, if the price drops, our put option will gain value. In either scenario, we profit as long as the price movement exceeds the cost of the options purchased.

While some traders rely on technical or fundamental analysis to forecast stock prices, many seasoned options traders appreciate the ability to profit without needing to predict future prices.

A market-neutral strategy like the long straddle focuses on forecasting the future implied volatility of a stock price. This approach can be more manageable than predicting price direction.

While stock prices can fluctuate widely, volatility tends to follow more rhythmic patterns. Academic research supports the notion that volatility clusters in the short term and mean-reverts over longer periods, providing opportunities for savvy traders.

The Long Straddle Option is Long Volatility

Being “long-volatility” in the options market means being a net buyer of options, or simply “long options.” The long straddle is a play on volatility rather than price, making the trade vega positive.

In the options market, an at-the-money (ATM) straddle best reflects the market’s estimation of future volatility, also known as implied volatility. To simplify, think of the ATM straddle as the over/under on volatility for that stock price.

Returning to our SPY example, here is the ATM straddle pricing for options expiring in 25 days:

SPY Long Straddle:

- BUY 1 396 Put @ $8.06

- BUY 1 396 Call @ 9.31

- Total trade cost: $17.37 (net debit)

With a trade cost of $17.37, SPY must move at least $17.37 in either direction within 25 days for us to profit. The assessment of whether this is a significant move depends on your trading skills.

Options traders consider various factors to determine if a straddle is appropriately priced, including current implied volatility compared to historical ranges, technical analysis, and anticipated market reactions to upcoming events.

Long Straddles Have Defined Risk

The long straddle involves buying a put and call option, which means the maximum risk is defined as the combined cost of the two options. This clarity provides a significant advantage, allowing traders to know their worst-case scenario.

In contrast, short options strategies, like the short straddle, carry unlimited and undefined maximum risk levels.

For this reason, long straddles are often among the first options spreads that novice traders explore beyond simply buying single put or call options. It’s similar to their previous experiences, but it eliminates the directional element.

Returning to our SPY example, the maximum loss in this scenario is $17.37.

The Long Straddle Has Unlimited Profit Potential

The long straddle offers theoretically unlimited upside profit potential. This means that if the underlying stock makes a significant move in either direction, profits can continue to grow indefinitely, except if the stock price drops to zero on the downside.

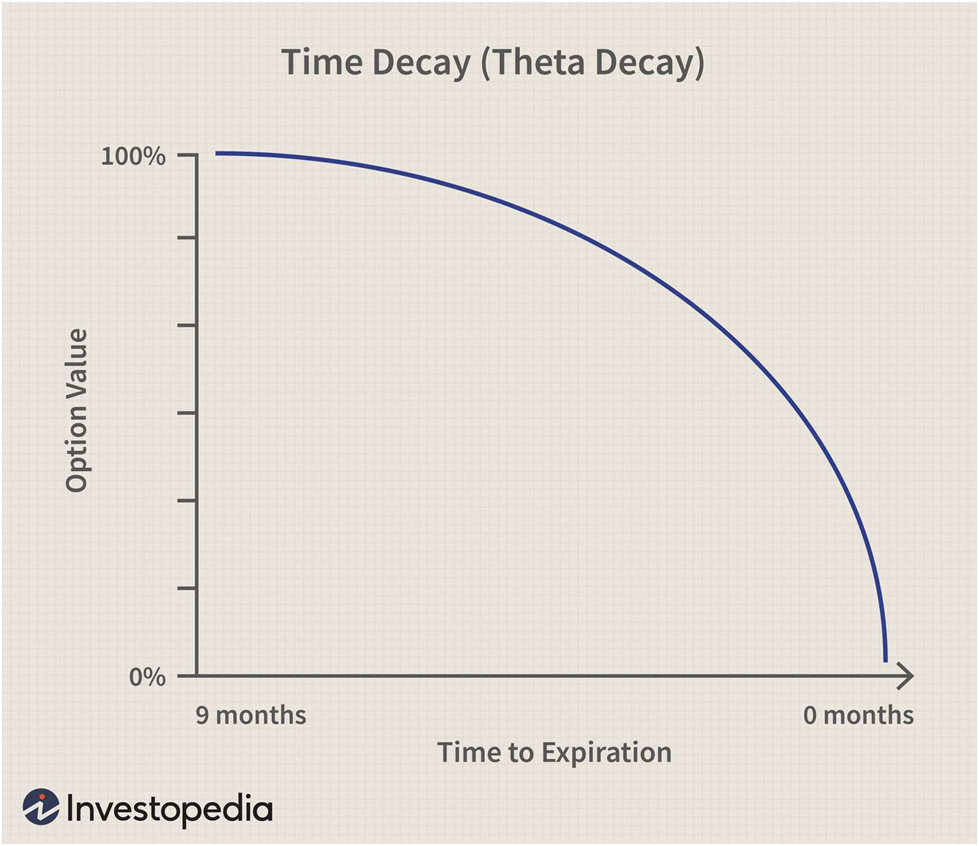

The Long Straddle Suffers from Time Decay (Short Theta)

When purchasing options, you’re essentially betting against time. The underlying stock price must make the desired move before the expiration date; otherwise, the options may expire worthless. This phenomenon is known as “time decay” or “theta decay.”

Theta is the Options Greek that measures an option position’s sensitivity to the passage of time. The beauty of the options Greeks is that they can be mathematically derived, allowing you to know precisely how much an option position will lose daily if all other factors remain constant.

Referring back to our SPY long straddle example, the position has a theta of -0.34, indicating it will lose approximately $0.34 in value per day until expiration. Note that theta changes over the life of an option; as the expiration date approaches, the value of theta declines due to reduced time value in the option.

Thus, while daily decay may decrease in absolute terms, it can often represent a higher percentage of the position’s value if the underlying stock price hasn’t moved favorably. The following chart from Investopedia illustrates this concept:

Source: Investopedia

How to Create a Long Straddle Position

The long straddle is one of the simplest options spreads available. It consists of a long put and call option. Here’s what a long straddle might look like on an options chain:

As illustrated, we’re buying a put and call option at the same strike price and expiration date. The example shows an at-the-money (ATM) straddle, but you can adjust the structure to align with your market view.

For instance, if we raise the strike prices of our straddle, it will become more profitable on the downside quicker, requiring a more significant price move for profitability on the upside. The opposite holds true as well.

Long Straddle Payoff and Max Profit/Loss

Long Straddle Breakeven Prices

The long straddle is straightforward for calculating breakeven, max profit, and max loss levels, making it an excellent spread for novices to explore in options trading.

Using our SPY long straddle as an example, we can calculate these levels:

SPY Long Straddle:

- BUY 1 396 Put @ $8.06

- BUY 1 396 Call @ 9.31

- Theta: -0.34

- Total trade cost: $17.37 (net debit)

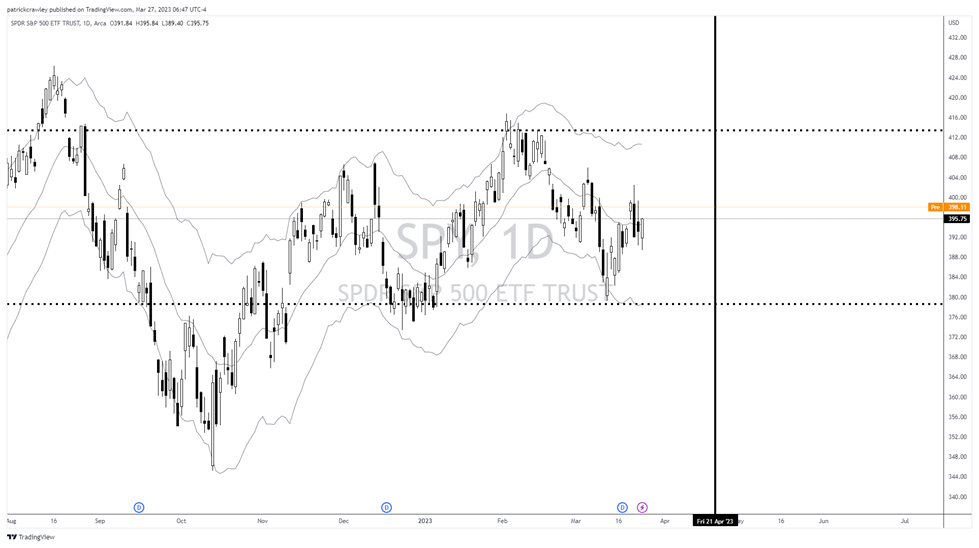

To calculate the upper breakeven price for a long straddle, simply add the total premium paid to the strike price. In this case, you add $396 + $17.37 = $413.37. Thus, our upper breakeven price is $413.37.

The lower breakeven price is calculated by subtracting the total premium paid from the strike price: $396 – $17.37 = $378.63.

To visualize these prices, here’s a chart of SPY:

The thick dotted lines indicate the upper and lower breakeven prices, while the vertical black line marks the expiration date. The price of SPY must exceed either of these levels for our hypothetical long straddle position to be profitable before expiration.

The maximum upside profit for a long straddle position is theoretically unlimited. There’s no cap on how high a stock price can rise.

Conversely, on the downside, your max profit is limited by the stock price. Since a stock can only drop to zero, you can calculate the max profit by subtracting the total premium paid from the strike price. In this case, the strike price is $396, and the total premium paid for our SPY long straddle is $17.37, leading to a max profit of $378.63, which aligns with our lower breakeven price.

Long Straddle Maximum Loss/Risk

The maximum risk for this position is simply the total premium paid. In our SPY straddle example, that amounts to $17.37.

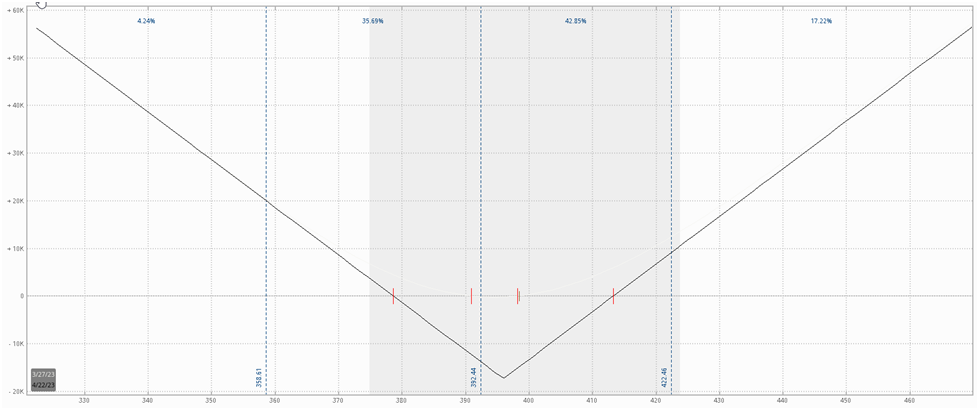

However, experiencing the absolute maximum loss in a straddle is rare, as demonstrated by the payoff diagram of the long straddle.

The long straddle payoff diagram typically exhibits a V-shape, contrasting with the flattened U-shape of the Long Strangle.

Here’s the straddle payoff diagram:

:max_bytes(150000):strip_icc()/understandingstraddles22-19b55dd41aee458287dda61e4929428a.png)

Let’s analyze a real-life example of a long straddle payoff diagram, using our SPY straddle as a reference.

As a reminder, here is our SPY long straddle position:

SPY Long Straddle:

- BUY 1 396 Put @ $8.06

- BUY 1 396 Call @ 9.31

- Theta: -0.34

- Total trade cost: $17.37 (net debit)

Long Straddle: Market View

Why Matching Your Market View to Options Trade Structure is Crucial

It’s essential to align your market view with the appropriate options spread. As an options trader, you are like a carpenter, and option spreads are your tools. If you need to tighten a screw, you wouldn’t use a hammer but a screwdriver.

Before adding a new spread to your toolbox, understanding the market view it expresses is crucial. One of the worst mistakes an options trader can make is structuring a trade that conflicts with their market outlook.

This mismatch often occurs with novice traders. For instance, if a meme stock like GameStop surged from $10 to $400 in a few weeks, a trader might believe the price will revert to its historical mean and decide to use options to express this view. However, novice traders often only have basic put and call options in their toolkit, leading to ineffective strategies.

In contrast, a more experienced options trader might employ a bear call spread to express a bearish view while also gaining short-volatility exposure. This trader can creatively structure trades to align with their market outlook.

The nuances of their view might lead them to add skew to the spread or convert it into a ratio spread.

What Market Outlook Does a Long Straddle Express?

A trader using a long straddle anticipates a significant increase in implied volatility and/or a substantial price movement while maintaining a neutral directional view.

Importantly, a trader purchasing a straddle should have a bullish outlook on volatility. Buying both an at-the-money (ATM) put and call option incurs a considerable premium outlay, so merely believing that volatility is cheap isn’t sufficient justification for buying a straddle. A significant price move is essential.

Additionally, it’s crucial to assess volatility in relative terms. While a 50% implied volatility might be high for a stock like Philip Morris (PM), it could be historically low for a stock like Tesla (TSLA).

When To Use a Long Straddle

There are numerous scenarios where a skilled options trader can profitably buy a straddle, but two primary situations warrant consideration.

The first is when implied volatility is at the lower end of its historical range, as measured by metrics like IV Rank.

The second is when an upcoming catalyst is anticipated, and the options market appears to be underpricing the associated volatility.

However, predicting event volatility can be challenging. It’s often more effective to exploit how options markets price event volatility over time rather than attempting to forecast market reactions to significant data releases. This point is particularly relevant when discussing pre-earnings straddles.

Buying Pre-Earnings Straddles

Earnings releases are a common scenario for straddle trading, occurring four times a year for most companies. A glance at a stock chart reveals that these one-day data releases often account for a significant portion of the stock’s annual price range.

Traders typically identify stocks with consistently underpriced earnings volatility. However, as the market adapts, volatility pricing tends to adjust accordingly.

One major challenge with earnings straddles is IV crush. Once the market digests the earnings report, implied volatility often plummets, as uncertainty surrounding the potential outcomes dissipates.

Moreover, the market frequently overprices earnings volatility.

For these reasons, at SteadyOptions, we prefer to trade pre-earnings straddles. As implied volatility (and, consequently, option prices) tends to rise leading up to earnings, we typically buy straddles 2-15 days before an earnings release and sell before the earnings announcement. This approach significantly mitigates the primary risk of the straddle strategy, which is negative theta.

Instead of betting on earnings outcomes, we combine momentum trading with the tendency for implied volatility to increase before earnings. This strategy exploits a repeatable trend in the options market, as evidenced by our performance page.

We first detailed this strategy in our article Exploiting Earnings Associated Rising Volatility.

Using Straddles to Trade Volatility Mean Reversion

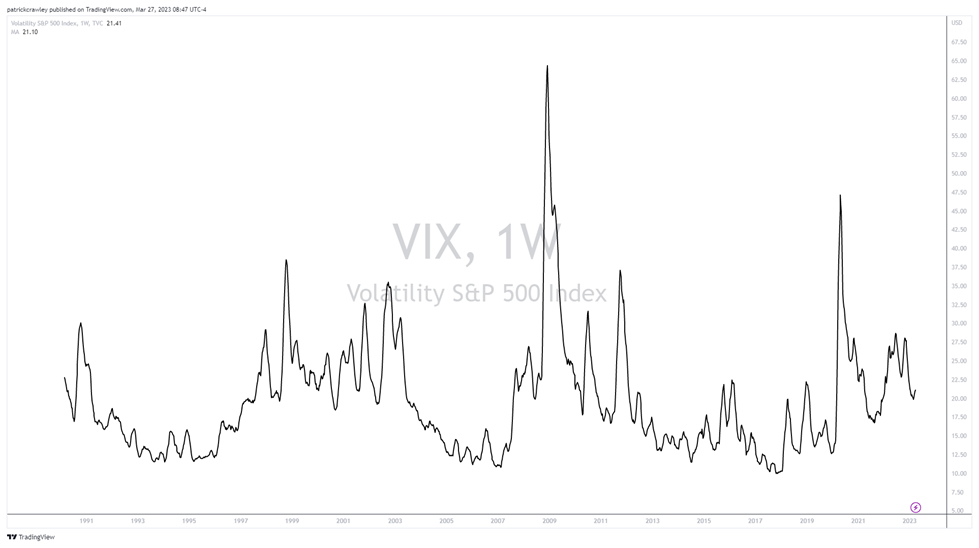

Volatility tends to expand and contract, resembling an EKG or sine wave rather than a traditional stock chart. For instance, consider the long-term moving average of the S&P 500 Volatility Index (VIX).

The following chart illustrates a 10-week moving average of the VIX since its inception in 1990:

There is clear mean-reverting behavior in this data. As mentioned earlier, this phenomenon is supported by academic literature in quantitative finance.

Options traders can exploit this behavior by waiting for periods when volatility is significantly low compared to its historical average. Various metrics, such as IV Rank, can be used to measure this.

To enhance potential gains, traders might also consider gamma scalping.

Long Straddle Options Spread Example

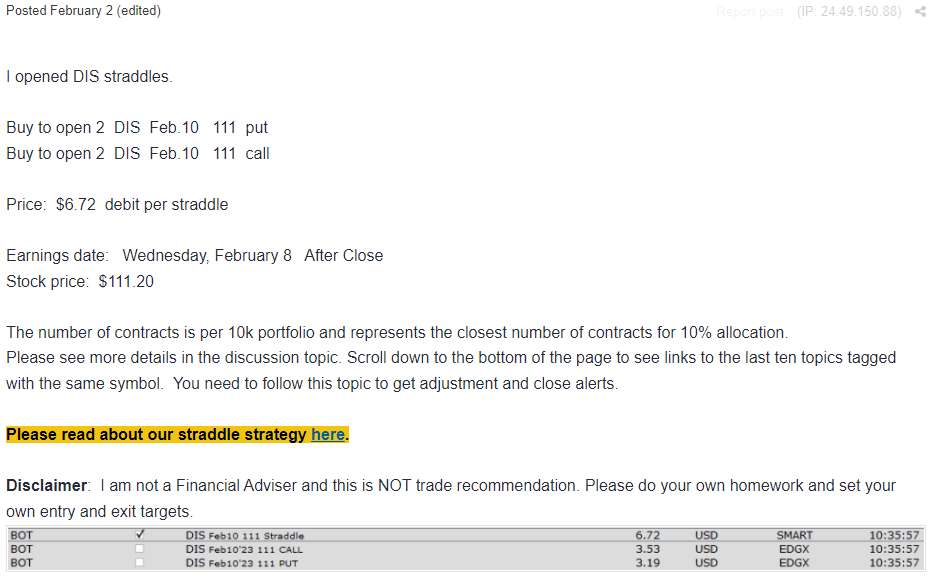

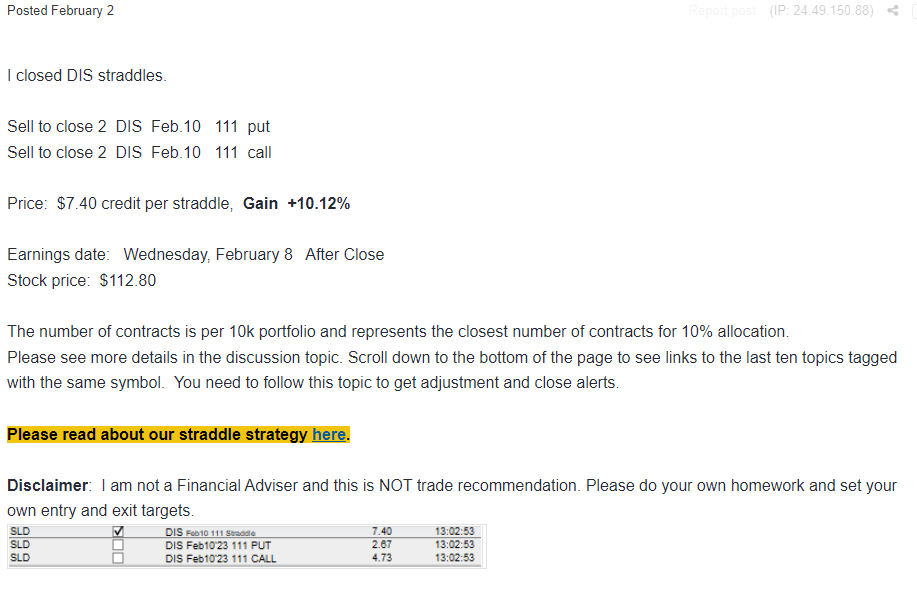

Here’s a recent example of our straddle strategy. DIS was set to announce earnings on February 8th, and we executed the following trade on February 2nd:

We paid $6.72 for the 111 straddle using options expiring on Feb.10 (2 days after earnings).

Three hours later, we closed the trade at $7.40, achieving a 10.12% gain.

The trade benefited from both stock movement and an increase in implied volatility.

Straddles Can Be A Cheap Black Swan Insurance

We favor trading pre-earnings straddles/strangles in our SteadyOptions portfolio due to their appealing risk/reward profile. There are three potential scenarios:

-

Scenario 1: The increase in implied volatility is insufficient to offset the negative theta, and the stock remains stagnant. In this case, the trade will likely incur a small loss, typically in the 7-10% range. It’s improbable to lose more than 10-15% on these trades if held for 2-5 days.

-

Scenario 2: The increase in implied volatility offsets the negative theta, and the stock price remains unchanged. Depending on the magnitude of the IV increase, gains could range from 5-20%. In rare instances, a dramatic IV increase could yield 30-40% gains.

- Scenario 3: The implied volatility rises, followed by a stock price movement. This scenario is where the strategy truly excels, potentially leading to significant profits.

The Biggest Risk When Buying a Long Straddle

Many traders buy straddles to capitalize on event volatility, betting that the options market is underpricing the risk of significant price movements in either direction.

However, everyone in the market is aware of the upcoming event. As a result, implied volatilities in post-event expirations tend to rise as the event approaches.

Yet, implied volatility often drops sharply once the event concludes and the market digests the results. This phenomenon is known as IV Crush, which we have discussed previously.

However, it’s crucial to emphasize this point. Numerous backtests indicate that holding straddles through earnings (the most common form of event volatility) is generally unprofitable. While some traders may successfully select their straddles, we prefer to focus on probabilities.

Instead, we exploit the tendency for earnings volatility to increase leading up to the event. However, instead of holding through the earnings release, we opt to sell before it.

This strategy of buying straddles 2-15 days prior to earnings and selling before the event is our core strategy. It can yield 5-10% gains in a short timeframe with limited risk while also serving as a form of black swan protection, as substantial gains can occur during unexpected events.

Bottom Line

The long straddle is a straightforward options spread involving the purchase of a put and call at the same strike price and expiration. However, simplicity does not equate to ease.

The essence of the straddle is a bet on significant change. A trader engaging in a long straddle is wagering on a substantial directional price move or anticipating that the options market will significantly raise volatility prices.

A long straddle option can be a viable strategy under specific conditions. However, be mindful that if there is no movement in stock price or implied volatility, the straddle will incur losses as expiration approaches. It should be employed judiciously, but when executed correctly, it can be highly profitable without necessitating directional predictions.

The following Webinar discusses different aspects of trading straddles.

Like this article? Visit our Options Education Center and Options Trading Blog for more.

Subscribe to SteadyOptions now and experience the full power of options trading at your fingertips. Click the button below to get started!