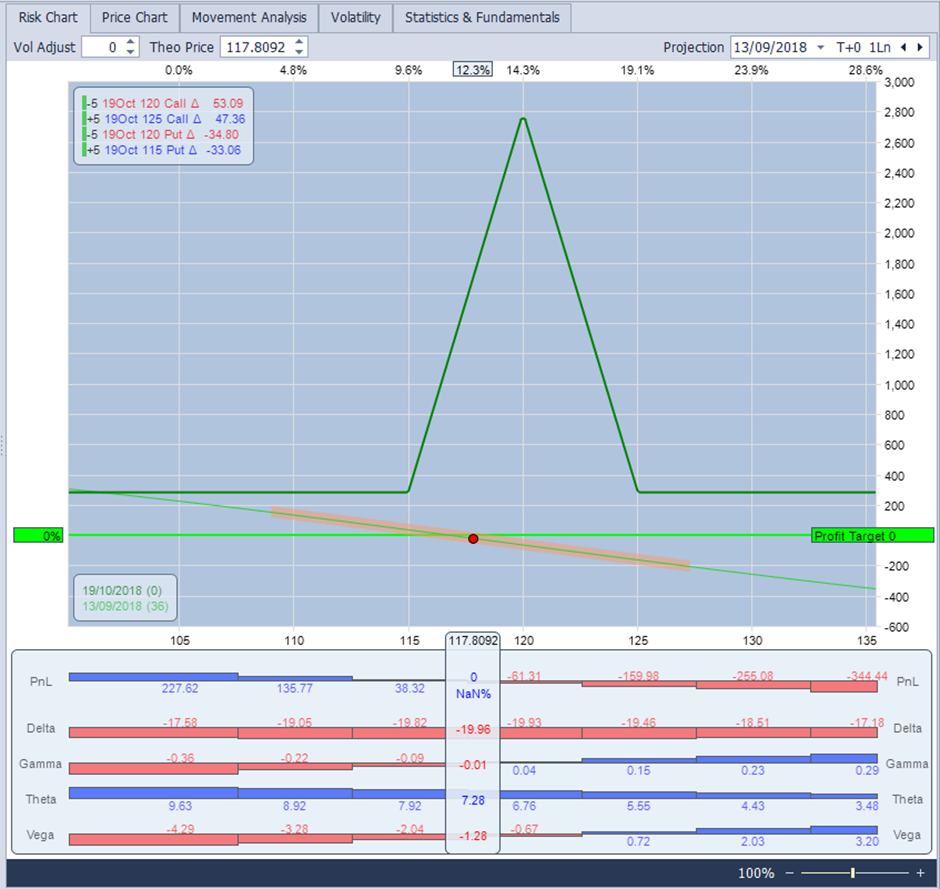

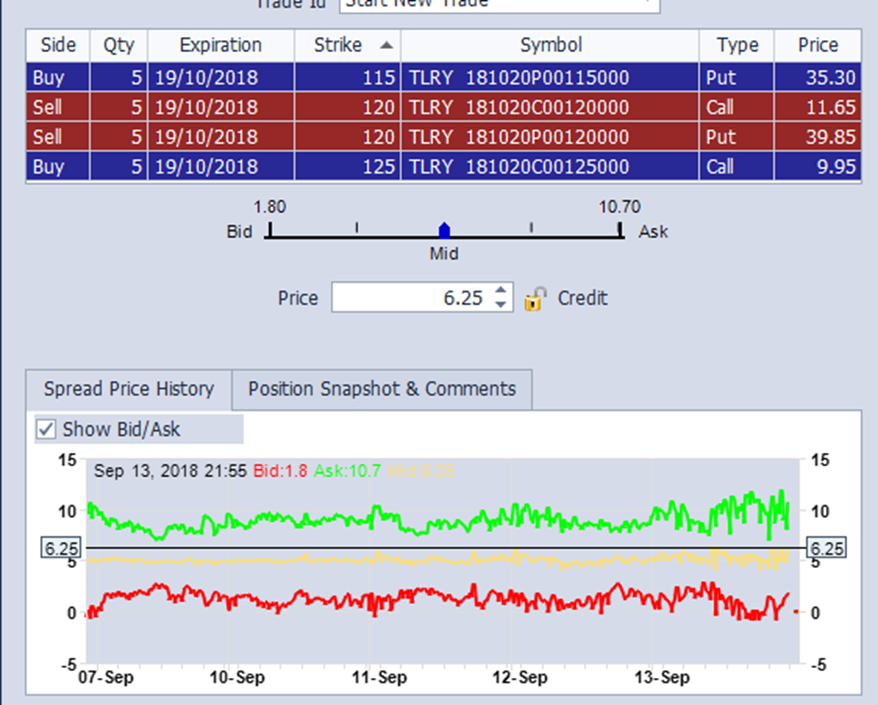

Figure 1 TLRY iron fly on 13 September 2018

Options trading offers a myriad of combinations, yet the classic risk-free trade often involves a credit spread where the wing width is smaller than the credit collected. Critics argue that in today’s algorithm-driven market, such pricing discrepancies are quickly eliminated. However, the chart above illustrates a real scenario where TLRY spreads maintained their pricing over an extended period, suggesting a potential “free lunch.”

Some may contend that market makers set spread differences, making it nearly impossible to enter or exit positions at theoretical profits. This argument can be countered by examining a recent unofficial trade on Steady Options involving DJT:

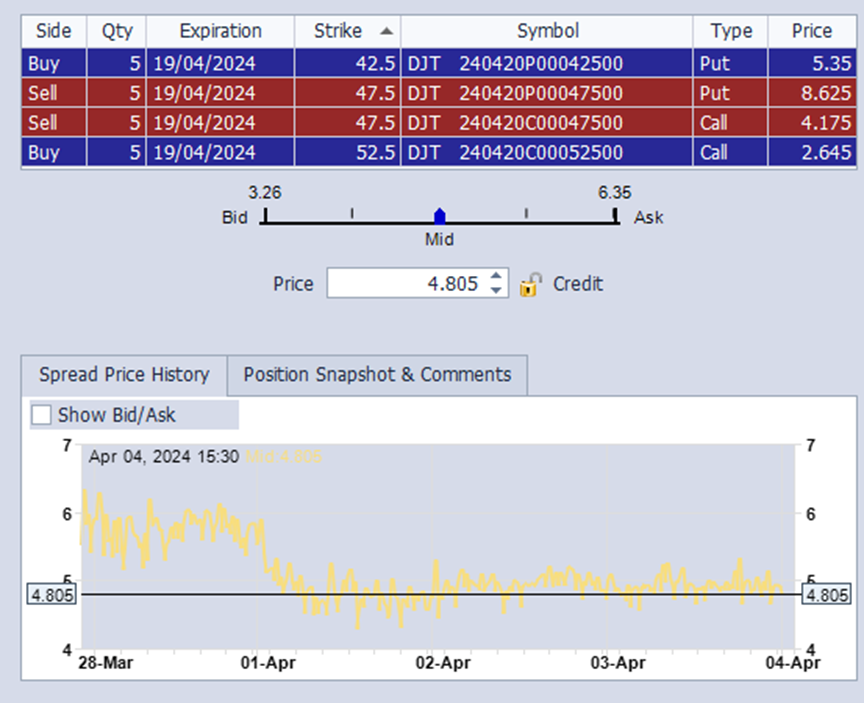

Figure 2 DJT iron fly on 4th April 2024

While the discrepancies in this case were less pronounced than in the TLRY example, the mid of this spread traded above $5, the width of the spread. Despite a wide bid/ask, significant trading occurred above this level. Such differences are typically expected at deep ITM or OTM levels due to skew, but they can occur in other scenarios as well.

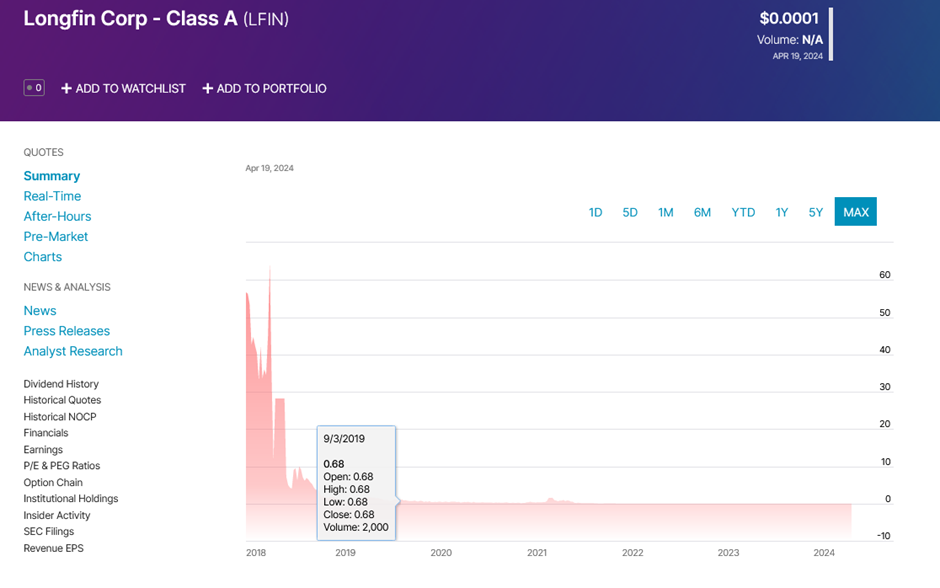

Of course, ‘haters are gonna hate’; many will argue that these mispricings yield only minimal profits. While trading and capital costs may limit gains, options, as leveraged instruments, can deliver substantial returns if you correctly predict market direction. The story of LFIN exemplifies this: once trading over $140, it plummeted to near zero, yielding some traders impressive returns of over 2000%.

Are you convinced yet? If so, you can buy us lunch!

In the following sections, we will explore the three trades mentioned and extract valuable lessons from them. While there may not be such a thing as a free lunch, there are opportunities to be seized with careful consideration.

When everybody was getting high

Butterflies are common options instruments, often balancing the net debit incurred in opening them against the width of the spread. A wide profit triangle can justify the risk of the stock ending outside your strikes. Typically, due to call/put parity, opening a credit spread for more than the width of the strikes is impossible. Market makers could exploit this pricing difference, quickly arbitraging it away.

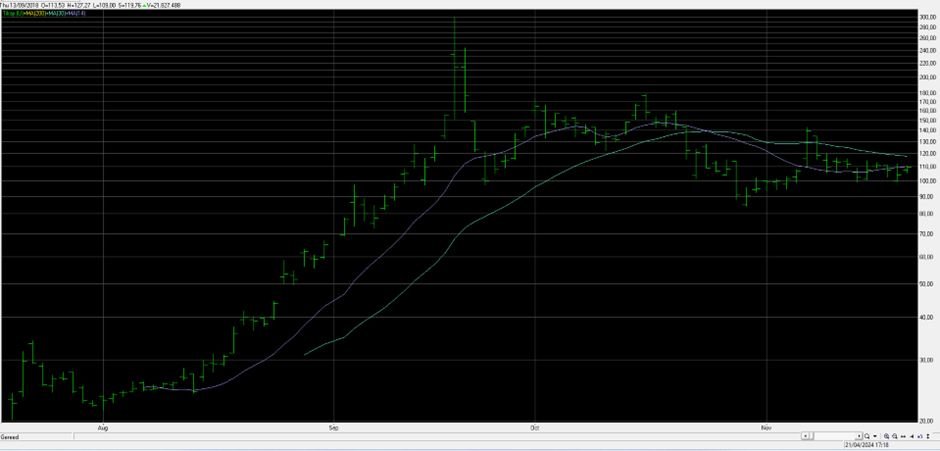

However, in 2018, a keen Steady Options member noted the meteoric rise of TLRY.

Figure 3 logarithmic TLRY stock from 07/2018 to 11/2018

This rise was accompanied by soaring implied volatility, with a staggering 70-point difference between the IV of ATM calls and puts. On September 13, 2018, the ATM $5 wide spread traded at over $6, reflecting market dynamics. Positions were opened at credits exceeding the width of the wings.

Figure 4 TLRY option spread ATM 13th September 2018 – 10 minutes before closing

Initially, it was presumed that this mispricing couldn’t last. Yet, it became evident that while opening positions at a credit above the wing width was feasible, closing them at the spread width was challenging. Traders noted that deeper ITM spreads were easier to open for decent credits. One trader opened 950 spreads across multiple strikes, a trade that could potentially secure retirement.

Doubts arose regarding hidden flaws, particularly concerning TLRY’s borrow rate.

Figure 5 Borrow rates for TLRY stock on 13th September 2018

As illustrated in Figure 3, TLRY’s rapid price movement necessitated a $120 cost for each ATM spread due to a 350% borrow rate. While the position was likely to yield surplus over the wing width, survival until expiry was crucial.

Traders began noticing that short calls were being exercised, presenting several tricky options:

- Exercise your long call (if ITM) and risk the stock not dropping to the put level;

- Borrow the stock and stay short at a cost of 1% per day;

- Close the entire position at a loss due to unreasonable put prices, especially since exercise occurs outside normal trading hours, adding volatility risk.

A further risk emerged: with significant stock movement, positions could end between strikes, locking in losses without allowing for profit realization. The weekend cost of carrying a short position could erase any potential gains.

The notion of a free lunch was misleading; the trader who opened 950 spreads faced a $27M risk, incurring four-digit losses on a few exercised spreads over a weekend. Some traders managed to exit before expiry, but the closer to Friday, the higher the risk of ITM calls being exercised.

The lesson learned was not that the trade was fundamentally flawed, but rather that options mispricing often signals underlying phenomena outside normal trading. In this case, factors included:

- The June 2018 agreement to legalize pot in Canada, effective mid-October;

- The recent IPO of TLRY, resulting in a narrow free float;

- The ‘meme-like’ euphoria surrounding pot stocks.

Key indicators from options trading included:

- Extreme volatility exacerbating price differences;

- Significant skew between calls and puts enhancing mispricing likelihood;

- Observing open interest in ITM calls indicating substantial exercising, despite new spreads being opened.

The position was vulnerable to early exercise, a characteristic of American-style options. Those not significantly ITM emerged relatively unscathed, but as TLRY hit $300 on September 19, 2018, nearly 50% of ITM calls with over a month until expiry were exercised.

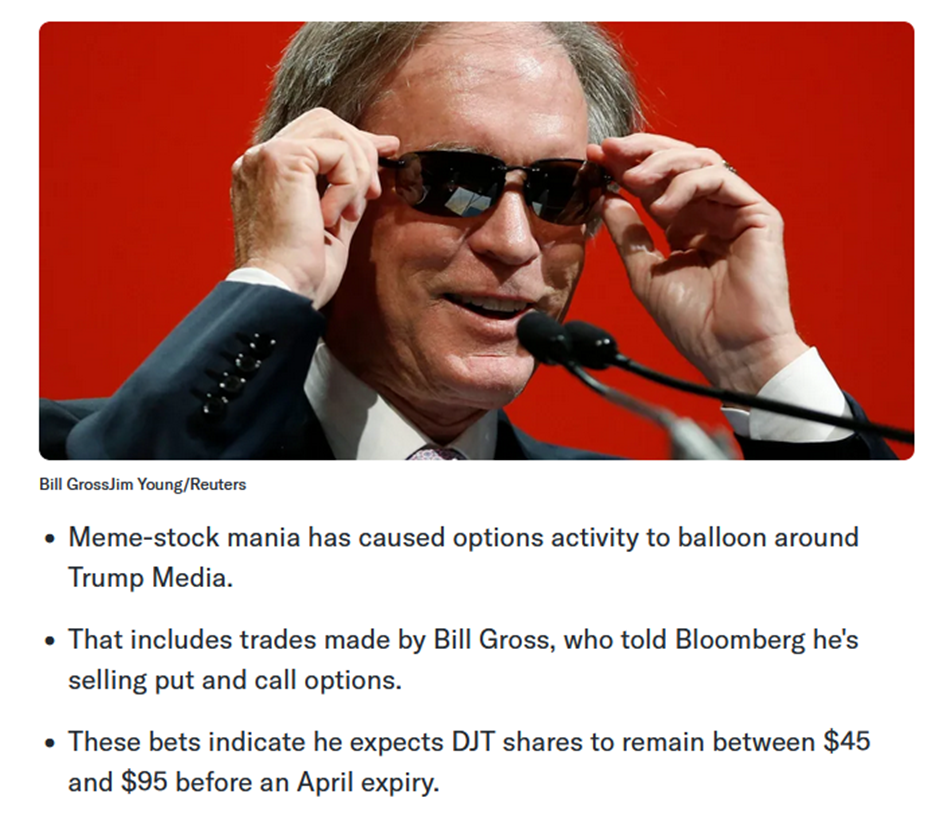

Bill Gross called it: If you are bold you sell premium on DJT

On March 29, 2024, DJT, Donald Trump’s social media company, launched on the stock market. Similar to TLRY, it garnered high visibility and mixed reviews. New Jersey businessman Mike Crispi epitomized the bullish sentiment.

A notable quote from Bond King Bill Gross stated, “A genius can have a high IQ or invest in the stock market during a bull market. A genius can also be an investor with the courage to sell DJT options at a 250 annualized volatility.” This likely mirrored a credit spread like an iron fly or condor, as Yahoo Finance reported:

DJT had huge volatility skew between puts and calls

Monthly options expiring in about two weeks showed the ATM put priced 2.4 times higher than the ATM call. This significant skew created a feasible arbitrage scenario. For instance, with the stock around $47.5, the 47.5/42.5 call and put credit spreads should cancel each other out, making it a nearly guaranteed break-even trade. However, in this extreme volatility skew, this combination could be opened for a credit exceeding the $5.00 wing width, ensuring a gain at expiration.

This trade yielded a $5.65 credit on a box combo with a $5.00 wing width, resulting in a guaranteed $65 profit at all stock price points at expiration.

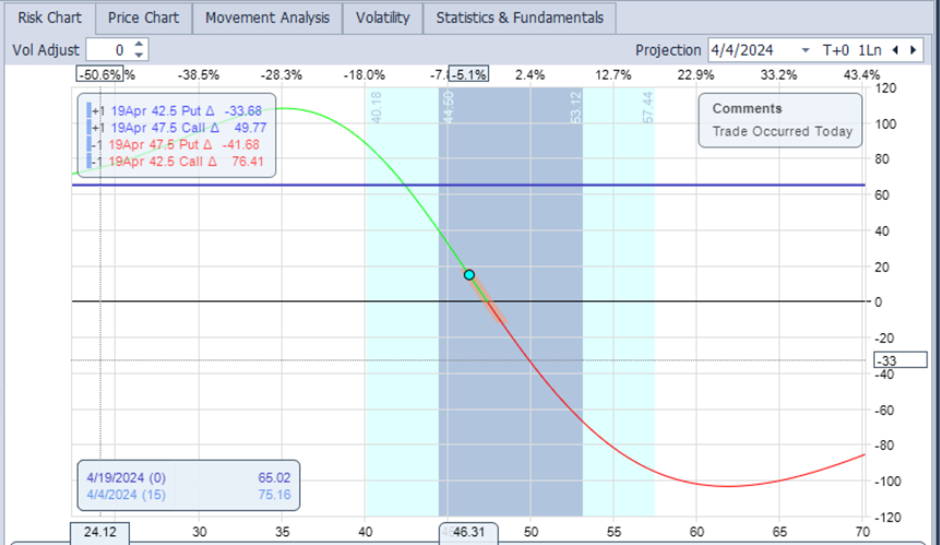

However, potential pitfalls existed due to early assignment risks with American-style options. The extreme put vs. call volatility skew that allowed this trade to be opened for a credit 13% above the wing width also created a delta-negative trade prior to expiration. Here’s the PNL chart at trade opening:

The thick blue line represents profit at expiration, showing $65 at all stock price points. However, the thin wavy line indicates a delta-negative trade, where PnL improves if the stock price drops but incurs losses if it rises. This occurs because the OTM put credit spread retains much of its value due to higher put IV.

If the stock price rises enough to reduce the short 42.5 call’s extrinsic value, the probability of assignment increases. In this case, you would need to close the call side near the $5.00 wing width while holding onto the put credit spread, hoping the stock price remains above 47.5 until expiration. This scenario carries significant risk, as the stock price could decline sharply with such high volatility.

Fortunately, in this trade, the stock price dropped, aligning with the trade’s direction. On April 15, four days before expiration, with the stock under $30, it was closed for a debit slightly under $5.00, generating a gain of just over $65. However, had the stock price risen, managing the trade would have been much more challenging. Ultimately, it turned out to be a free lunch trade, but only because the stock price cooperated.

The lead balloon that was LFIN

One of the appealing aspects of options is the ability to express market views without risking everything, while still having the potential for infinite returns. The story of LFIN, a crypto pioneer, exemplifies this. The mispricing traders exploited, which later led to their dismay, stemmed from events that rarely impact traditional stocks:

- A meme-like enthusiasm for crypto;

- A stock market launch backed by NASDAQ’s strict rules, yet with a limited free float;

- The announcement of an investment in a nascent crypto platform;

- A rare misstep by FTSE Russell Index managers who included the stock in their index without adhering to their own rules.

These factors propelled the stock from $5 to over $140, resulting in billions in market valuation. A critical issue arose when the amount of stock required for index funds exceeded half the inflated free float, leading to a bona fide short squeeze.

As the frenzy peaked, CEO Venkata Meenavalli appeared on CNBC, where the stock price plummeted 16% in after-hours trading as viewers witnessed the decline in real-time.

Figure 7 LFIN CEO interview on CNBC 18th December 2017, with live AMC prices as he speaks

A few memorable quotes from the interview included:

- Q: How many bitcoin transactions have you done?

A: We own 140 bitcoins; - ‘We are a profitable company.’ and ‘We are the GEICO of this world.’

- ‘We have a team of quants.’

- Q: ‘Is the $6B market valuation absurd?’

A: ‘Yes.’ - Repeatedly stating: ‘You have to understand that…’ followed by unintelligible remarks.

Unsurprisingly, option traders flocked to buy puts, with retail traders on Reddit holding positions ranging from 10 to hundreds of put options at various strikes. Here’s what transpired with LFIN:

The chart’s insanity is undeniable; LFIN listed at $5 on December 15, 2017, and soared to $142 (closing at $72.38) by December 18, 2017, coinciding with the CEO’s disastrous interview. This situation presented a compelling case for buying puts, especially as Citron Research and others exposed the company as a scam. As March approached, LFIN faced SEC investigations, and FTSE Russell reversed its decision to include the stock in their index, leading to multiple lawsuits and NASDAQ inquiries.

A T12 notice was issued at the end of March, effectively delisting the stock. This created a trifecta of challenges for put holders, particularly those with deep ITM positions opened at $5 for the April expiry:

- Institutional holders owning 45% of the theoretical free float were unable to unload their stock;

- The CEO misrepresented the free float, leading NASDAQ to halt 26M shares from circulation;

- Short sellers and put holders held over 250% of the free float, creating an inverse short squeeze.

As institutional holders faced millions in losses, borrowing costs skyrocketed to 3000%. Put holders had to exercise their options and hope trading would resume to cover their shorts. Historically, T12 trading halts have lasted over three months, placing April, May, and June put option holders in a precarious position.

Exercising puts required covering the full value of the shares, a significant burden for call holders with strikes around the money. Put holders faced exorbitant borrowing fees without knowing when they could cover their shorts. Trading resumed OTC on May 28, 2018, but it took another month for the stock to drop below $5, leaving those who exercised $2.50 strike puts in a difficult situation.

Many retail traders reported that even those who initially profited ended up losing six figures after doubling down. As the owner of this website famously stated, position sizing is crucial for successful trading.

What shall we have for lunch?

The stock market adages that ‘there is no such thing as a free lunch’ and ‘the market can stay irrational longer than you can stay liquid’ exist for a reason. Mispricing in options and opportunities for arbitrage do occur, primarily in unusual situations where risks differ from trading established and liquid stocks. Black swan events, such as trading halts, often remain misunderstood until faced directly.

Should you avoid trading these opportunities? Absolutely not; where’s the excitement in that?

However, it’s essential to recognize the risks involved and size your positions accordingly. Be prepared to take quick profits rather than waiting for a perfect outcome. If tempted to make a YOLO trade, remember the cautionary tale of the ‘Man who couldn’t lose.’ His secret? ‘Observe the room until you find the guy about to lose everything. Bet against him, because that guy ALWAYS loses.’ The same applies to any YOLO or retirement trade; greed often leads to failure, while a more measured approach could have you joining us for lunch at Taco Bell.

Many thanks to our contributors @TrustyJules and @Yowster for this fascinating article.