In the ever-evolving tech landscape, even the most beloved companies can find themselves in a precarious position with investors. Growth may stall, risks can escalate, and the spotlight often shifts to newer trends. However, amidst this turbulence, some firms continue to provide reliable dividend growth. Let’s delve deeper into one such company.

Built for Ecosystem Domination

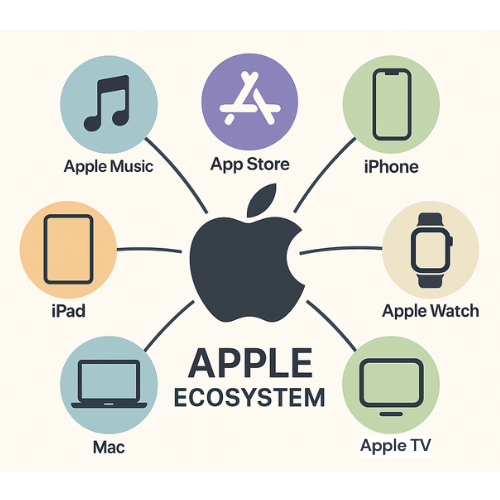

This company has become a hallmark of sleek design, user-friendly software, and a loyal customer base. Its revenue streams are derived from a blend of premium hardware and subscription services that seamlessly integrate into users’ everyday lives.

From smartphones and wearables to digital content and payment systems, it has crafted a comprehensive experience that fosters customer loyalty. The hardware attracts users, while the services ensure they remain engaged—and the profit margins benefit from both.

With a strategic focus on custom silicon for enhanced performance and battery life, alongside platform control through services like the App Store and Apple Pay, this company transcends being merely a product provider. It has evolved into a self-sustaining ecosystem that also offers dividends.

Services Spotlight: Where Growth Hides

While the growth narrative may no longer hinge on iPhone sales, the Services segment is emerging as the crown jewel of this tech empire. With offerings like iCloud, AppleCare, and the App Store, Services generated over $26 billion in quarterly revenue, marking a record high with 12% year-over-year growth. This segment boasts gross margins exceeding 70%, significantly outpacing hardware, and provides the predictability that investors cherish.

The incorporation of “Apple Intelligence” into apps such as Mail, Messages, and Siri could enhance user engagement across subscriptions. Whether it’s Fitness+, News+, Music, or iCloud+, Apple’s ecosystem functions as a digital tollbooth—small recurring fees that accumulate into substantial cash flow. In an era of slowing device growth, this pivot towards monetizing a vast user base exemplifies strategic reinvention.

When Growth Slows, Is the Core Still Strong?

Bull Case: Monetizing the Base

Apple stands as one of the world’s most valuable companies, and rightly so. The transition from hardware growth to service monetization is well underway, with Services now accounting for over 25% of total revenue and continuing to grow in double digits.

The latest push for “Apple Intelligence” aims to keep users engaged and encourage upgrades, particularly with older models like the iPhone 16e. Additionally, growth in markets like India and Southeast Asia indicates that the user base is still expanding.

The tight integration of hardware and software enhances profit margins, and it’s important to remember that this company operates as a cash machine with an ecosystem moat that is broader than most.

Bear Case: Too Big to Sprint?

Despite its strengths, Apple faces significant pressure. iPhone sales still account for over 50% of revenue, exposing the company to market saturation, geopolitical tensions (particularly concerning China and Taiwan), and regulatory scrutiny aimed at dismantling its ecosystem dominance.

The wearables market has cooled, and competitors like Microsoft and Google are making strides in AI innovation. Furthermore, the Vision Pro may be more of an “early tech demo” than the anticipated “iPhone moment.” As one analyst noted, “It’s been a few years since Apple delivered that high single to double-digit growth investors came to expect.”

Want to Build a Dividend Income Stream for Life?

The Dividend Income for Life Guide provides insights on generating safe, growing income year after year. Whether you’re just starting or refining your portfolio, this guide outlines proven strategies and timeless principles.

Get your copy here

What’s New: iPhone Sales Steady, Services Shine

In the latest quarterly results (May 2025), expectations were surpassed, though the growth narrative is becoming increasingly uneven:

-

Revenue: +5% YoY

-

EPS: +8% YoY

-

Services: Record $26.65B, up 12%

-

iPhone: +2% YoY, aided by iPhone 16e

-

Mac: +7%, iPad: +15%

-

Wearables & Home: -5%, indicating market saturation

While Services achieved a record-breaking quarter, Apple’s wearables segment is experiencing a slowdown, and the focus remains on AI and innovation—areas where competitors are gaining traction.

The Dividend Triangle in Action: Modest but Reliable

Let’s analyze the situation through the lens of our Dividend Triangle:

-

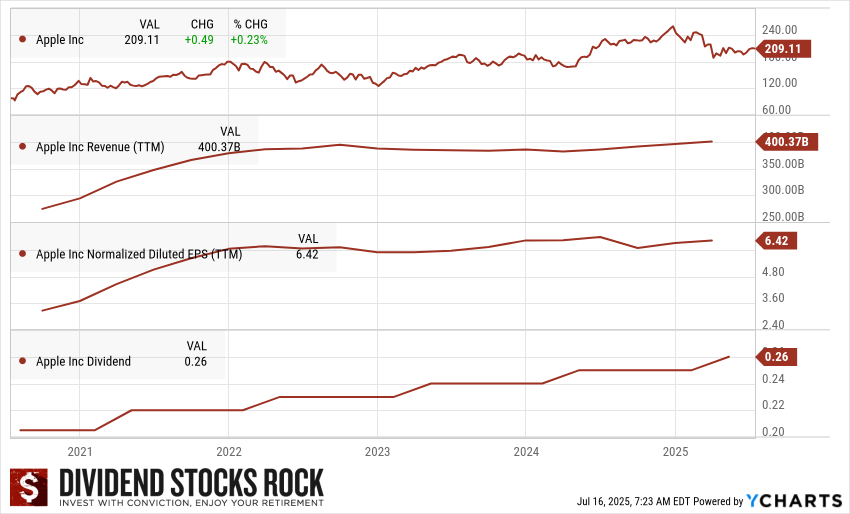

Revenue Growth: Now exceeding $400 billion annually, although growth is slowing.

-

Earnings Growth: EPS stands at $6.42, showing a slight increase from last year.

-

Dividend Growth: Recently increased to $0.26 per share, with consistent low-single-digit hikes.

While the yield remains modest, the payout is secure and on an upward trajectory. Apple tends to return value through buybacks, yet the dividend trend remains steadfast.

Final Words: Quiet Power, Loud Headlines

This isn’t a high-yield investment or a screaming buy. However, for those seeking stability, predictability, and a cash-rich business with a history of rewarding shareholders, it still warrants a place on your watchlist.

The market’s preoccupation with AI disruption, regulatory challenges, and geopolitical risks may dampen sentiment. Yet, it’s often during such times that a reliable compounder excels.

The Best Guide to Creating a Sustainable Dividend Income at Retirement

This guide is designed for any investor aiming to create a sustainable income from their portfolio. It proves invaluable during the accumulation phase, helping avoid major pitfalls while building a solid retirement portfolio. It’s equally beneficial for retirees relying on their investments to cover expenses.

Ultimately, we all invest with the same goal: to have our money working for us.