Investors have long viewed consumer staples as reliable anchors in their portfolios. While these businesses may not offer explosive growth, they typically navigate economic storms more effectively than their flashier counterparts. However, they are not immune to short-term challenges, particularly when sales volumes decline and profit margins are squeezed. Let’s explore a household name that has faced recent pressures, yet continues to exemplify why it remains a classic choice for dividend growth.

Built on Snacks and Sips

PepsiCo (PEP) is much more than just a soda company. It stands as a global food-and-beverage titan, boasting a brand portfolio that includes everything from Doritos and Lay’s to Gatorade and Quaker Oats. The company’s operations are divided between convenience foods, which account for about 55% of sales, and beverages, making up the remaining 45%.

-

Snacks: Frito-Lay North America leads the savory snack market with popular brands like Lay’s, Cheetos, Doritos, and Ruffles.

-

Beverages: This segment includes carbonated soft drinks (Pepsi, Mountain Dew) and non-carbonated options like Gatorade, Starbucks ready-to-drink coffee, and Aquafina.

-

Global Reach: PepsiCo operates across North America, Latin America, EMEA, and APAC, providing a level of geographic diversification that few competitors can match.

-

Integration: A vertically integrated supply chain and direct-store-delivery model ensure shelf dominance and operational efficiency.

When a Snack Giant Faces Pressure

Bull Case – Brands That Endure

PepsiCo’s strength lies in its diversified portfolio and global scale. Even during challenging times, the company benefits from consistent demand for its core products and pricing power derived from strong brand loyalty.

-

Resilient Demand: Snacks and beverages are everyday staples, providing a predictable revenue stream.

-

Balanced Model: By offering both snacks and beverages, Pepsi can bundle products for retailers, securing premium shelf space.

-

International Growth: Emerging markets, particularly in India, Latin America, and the EMEA region, continue to drive strong growth.

-

Product Evolution: Acquisitions like Siete Foods and Poppi allow PepsiCo to tap into healthier consumer trends.

-

Moat: Its scale in logistics, retail leverage, and marketing creates significant barriers for competitors.

Bottom line: PepsiCo continues to provide long-term revenue stability, with innovation and international markets fueling its growth engine.

Bear Case – Volumes Don’t Lie

Despite its advantages, PepsiCo is not immune to changing consumer habits or rising costs.

-

Soft Volumes: Since 2023, U.S. snacks and beverages have experienced approximately 2% volume declines, reflecting inflationary pressures on consumers.

-

Margin Compression: Increased selling, general, and administrative expenses, along with commodity inflation, have reduced operating margins from 18% in 2022 to below 8% in 2025.

-

Regulatory Risks: Anti-sugar and anti-salt legislation could pose challenges for both beverages and snacks globally.

-

Competitive Pressures: Coca-Cola remains a leader in beverages, while Mondelez and General Mills compete for snack dominance.

-

Currency & Global Risk: International strength is somewhat offset by foreign exchange volatility and geopolitical uncertainties.

Bottom line: The decline in North American volumes and profitability explains the downward drift of shares since their 2023 highs, despite solid international growth. Investors are concerned about Pepsi’s ability to regain domestic momentum.

Free Webinar: Avoid Price Confusion

When a stock experiences a significant drop or spike, many investors react to the price change. However, successful investors know the importance of thoroughly examining the business first.

👉 Join our free webinar on Thursday, September 18 at 1:00 p.m. ET:

-

Learn a simple framework to determine when to ignore headlines and when to pay attention.

-

Utilize the Dividend Triangle to differentiate between bargains and traps.

-

Gain a repeatable method to invest with confidence.

Seats are limited to the first 500 attendees. Can’t attend live? No worries — a replay will be sent to all registrants.

Save your spot (or get the replay): dividendmonk.com/webinar

What’s New: Mixed Results in Q2 2025

PepsiCo’s latest quarter showcased both its strengths and vulnerabilities:

-

Revenue: Increased by 1% year-over-year, bolstered by 7% growth in EMEA and 5% in International Beverages.

-

EPS: Decreased by 5% year-over-year, as operating margin contracted to 7.9% from 18%.

-

North America: Volumes for Frito-Lay and PepsiCo Beverages softened by approximately 2%, indicating a pullback from U.S. consumers.

-

International: Strong performance in Latin America and EMEA helped offset domestic weaknesses.

-

Guidance: The 2025 outlook has been reaffirmed, demonstrating confidence despite ongoing cost pressures.

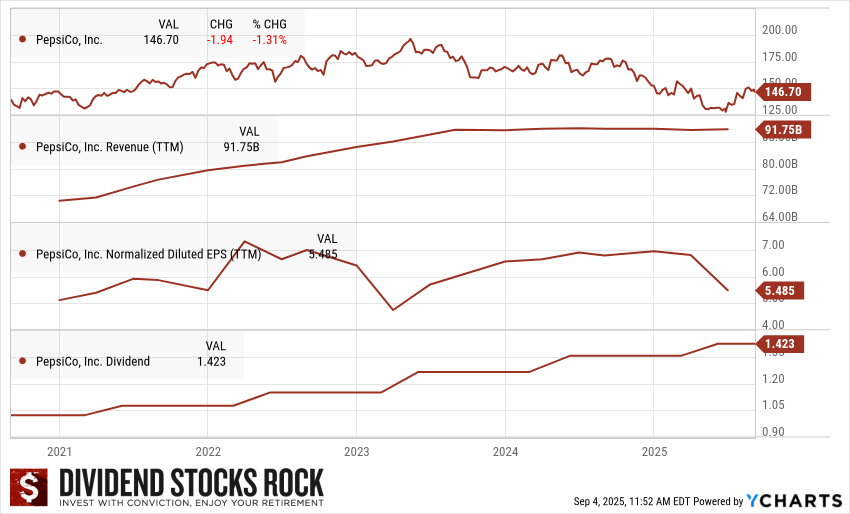

The Dividend Triangle in Action: Stability with Slower Growth

PepsiCo’s dividend triangle, which encompasses revenue, EPS, and dividend growth, illustrates a business that is still growing, albeit at a slower pace:

-

Revenue: Steadily climbing, reaching nearly $92 billion TTM, with international markets driving most of the gains.

-

EPS: Currently around $5.5, down from higher levels in 2022–23 due to margin pressures.

-

Dividend: Consistently growing, now at $1.42 quarterly, reflecting Pepsi’s commitment to income-focused investors.

The dividend continues to grow even as earnings face pressure — a testament to PepsiCo’s stability, but also a reminder of the margin challenges it must address to sustain future increases.

Final Words: Why Patience Matters

PepsiCo may not be a high-growth stock at the moment. North American volumes remain soft, and profitability has clearly declined since 2023, which explains the stock’s recent pullback. However, for patient investors, Pepsi’s international expansion, brand loyalty, and pricing power still position it as a reliable income generator. While dividend growth may be modest in the short term, the long-term outlook for resilience and global relevance remains strong.

Secure Your Webinar Seat

Market fluctuations can easily unsettle even the most disciplined investors. This upcoming session is particularly timely.

- Free Webinar: Avoid Price Confusion and Act with Conviction

- Thursday, September 18th at 1:00 p.m. ET

- Replay available for all registrants

If you’re uncertain about whether to sell, hold, or buy after earnings announcements, this webinar is for you.

Register now: dividendmonk.com/webinar