Diagonal spreads resemble vertical spreads in that the objective is to have them move In-The-Money (ITM). A long diagonal spread essentially combines a vertical spread with a longer-term long option. This structure allows for a maximum profit that can exceed the width of the diagonal spread, as the short option expires before the long option.

The long option retains extrinsic value as the short option expires, which is a key aspect of this trade. It functions similarly to a vertical spread but has the added potential for an extrinsic value boost from the long option.

If a long diagonal spread is showing a loss, it indicates that the spread is moving out-of-the-money (OTM), causing both the long and short options to lose value. Given the time difference between the long and short options, various defensive tactics can be employed to hedge and reduce the cost of the remaining long option. This may involve rolling the short option out in time, moving it closer to the long option’s expiration, or a combination of both strategies.

Diagonal Bull Call Spread Construction

- Buy 1 Long-Term ITM Call

- Sell 1 Near-Term OTM Call

Limited Upside Profit

The optimal scenario for a diagonal bull call spread buyer occurs when the underlying stock price remains stable or rises beyond the strike price of the sold call by the time the long-term call expires. In this case, once the near-month call expires worthless, the options trader can write another call, repeating this process monthly until the expiration of the longer-term call, potentially allowing them to hold the long-term call “for free”.

Under these ideal conditions, the maximum profit for the diagonal bull call spread equals the total premiums collected from writing the near-month calls, plus the difference in strike prices of the two call options, minus the initial debit incurred to establish the trade.

Limited Downside Risk

The maximum potential loss for the diagonal bull call spread is confined to the initial debit paid to establish the spread. This occurs when the stock price declines and remains low until the expiration of the longer-term call. Long put and call diagonal spreads are defined risk strategies, where the maximum loss is the upfront debit if the long option expires worthless. Losses can occur before expiration if the stock moves unfavorably, pushing the spread further OTM and eroding the extrinsic value of both options.

The short option in a diagonal spread serves to hedge against the cost of the long option and unfavorable price movements. However, since the short option is worth significantly less than the long option, this hedge is temporary. If the short option has lost most of its value or has expired, another short option can be sold against the long option to continue reducing the cost basis. It’s crucial to monitor the width of the spread to ensure that the net debit does not exceed the spread width if the short strike is adjusted closer to the long strike.

The spread can be closed prior to expiration for less than the maximum loss if the trader’s outlook changes or if they believe the spread will not return to ITM before the long option expires.

Example

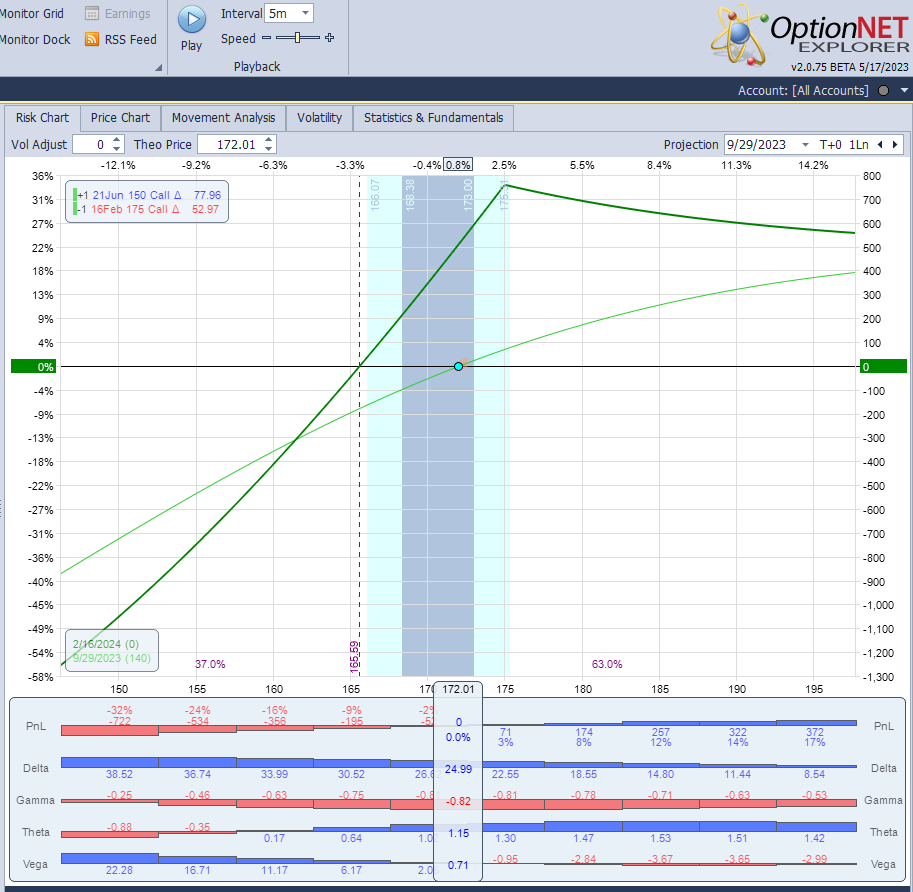

An options trader anticipates that AAPL stock, currently trading at $172, will gradually rise over the next four months. To capitalize on this, they enter a diagonal bull call spread by purchasing a June 2024 150 call and writing a February 2024 175 call, resulting in a net investment of $2,200.

This is how the P/L chart looks like:

If the stock price of AAPL rises to $175 within the next four months, the options trader can write another call of the same or slightly higher strike as each near-month call expires.

Time Decay Impact on a Diagonal Spread

Time decay, or theta, positively affects the front-month short call option while negatively impacting the back-month long call option in a call diagonal spread. The goal is for the short call option to expire out-of-the-money. If the stock price is below the short call at expiration, the contract will expire worthless, benefiting from the passage of time.

The effect of time decay on the back-month option is less pronounced early in the trade, but the theta value will increase rapidly as the second expiration approaches, potentially influencing the decision to exit the position.

Adjusting a Diagonal Spread

Call diagonal spreads can be adjusted during the trade to increase credit. If the underlying stock price declines sharply before the first expiration date, the short call option can be repurchased and sold at a lower strike closer to the stock price, collecting more premium. However, this adjustment increases risk due to the spread width between the near-term and long-term expiration contracts if the stock reverses. If the short call option expires out-of-the-money and the investor wishes to retain the long call, a new position can be established by selling another short call option.

The ability to sell a second call contract after the near-term contract expires or is closed is a crucial aspect of the call diagonal spread. The spread between the short and long call options should maintain at least the same width to avoid additional risk. Selling a new call option will generate more credit and may even lead to a risk-free trade with unlimited upside potential if the net credit received exceeds the width of the spread between the options.

Assignment Risk

A common question arises: what happens if the stock rises and the short calls become ITM? Is there an assignment risk? The answer is that assignment risk becomes significant only when there is minimal time value left in the short options, typically when they are deep ITM and nearing expiration. In such cases, rolling the short options or closing the trade may be necessary. However, this is manageable since even if assigned short stock, the position is hedged by the long calls.

In the event of an upcoming dividend, assignment risk is present only if the remaining time value of the short calls is less than the dividend value. There is no assignment risk if the calls are OTM or around ATM.

Related articles: