This article explains how implied volatility (IV) can influence your trading decisions, particularly regarding the types of trades you choose to open.

Directional Spreads

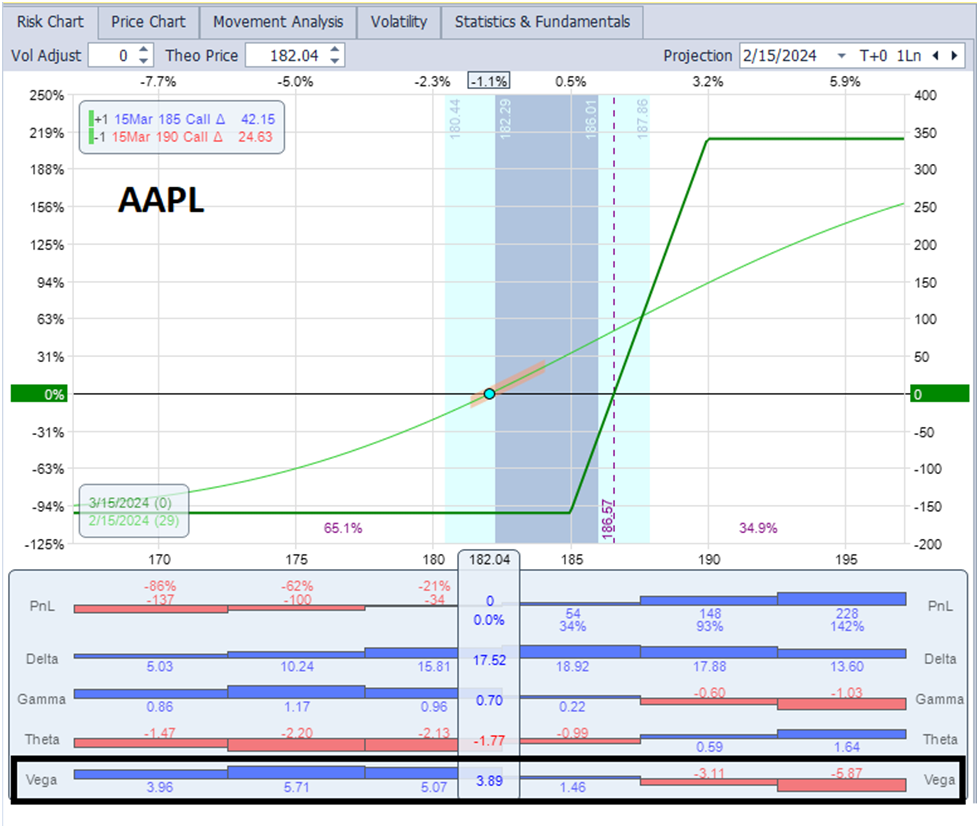

Let’s begin with one of the simplest options spreads: the put or call vertical spread. This strategy is often employed to capitalize on a stock’s movement in a specific direction. For example, consider a slightly OTM (Out of The Money) call vertical debit spread on AAPL, set to expire in about a month. The stock price is $182, and the spread involves a long position in the 185 call and a short position in the 190 call. Pay attention to the highlighted Vega section, which illustrates key points regarding IV:

- When the spread strikes are OTM (the stock price is below both long and short call strikes), the trade is vega positive. This means that while the spread remains OTM, an increase in IV will help it retain more of its value.

- As the stock price rises toward the spread strikes, the degree of vega positivity diminishes. It eventually becomes vega neutral at approximately the break-even point for the spread at expiration.

- As the stock price continues to rise, approaching the higher short strike and beyond, the trade becomes vega negative. In this scenario, when the spread is ITM (In The Money), a decrease in IV will help the value get closer to the spread width (the maximum gain).

How does this factor into your trade opening decision? When initiating a bullish call vertical spread during elevated IV, it may be beneficial to enter near the vega neutral position, with the long strike ITM and the short strike OTM. This setup typically results in a scenario where the maximum gain is equivalent to the maximum loss. If the stock price rises, you will reach the point where the spread becomes vega negative sooner, meaning any drop in IV won’t be detrimental. Conversely, if you open the trade when IV is lower, you can start with both legs of the call vertical being OTM. This configuration allows for a higher maximum gain compared to the maximum loss, while also reducing the risk associated with further declines in IV.

Spreads for Minimal Stock Price Movement

Now, let’s focus on common spreads designed for minimal stock price movement. The Iron Condor (IC) is a prime example. It consists of both an OTM put credit spread and an OTM call credit spread. When the stock price is positioned between the wings, it is vega negative, meaning a drop in IV will accelerate profit growth beyond what time decay alone would generate. Conversely, an increase in IV will decelerate profit growth.

How does this impact your trade opening decision? Opening an IC when IV is low means you’ll need to use strikes closer to ATM to achieve the same opening credit compared to times when IV is higher. Additionally, when initiating with low IV, a further decline is less likely, so you won’t benefit from accelerated profit growth if IV drops. Conversely, opening an IC when IV is elevated allows you to use farther OTM strikes, requiring a larger stock price move to reach the losing zones. Any decline in IV can accelerate profit growth, provided the stock price remains stable.

Many traders shy away from Iron Condors due to their risk versus reward, where the maximum loss exceeds the maximum gain. Let’s explore two other common spreads for minimal stock price movement that offer a more balanced risk-reward profile: the calendar spread and the butterfly spread. The calendar spread typically utilizes the ATM strike and primarily benefits from theta decay and minimal stock price movement. It is vega positive across the board, meaning rising IV will enhance the trade’s potential gains and widen the profit tent.

The butterfly spread also features a balanced risk-reward profile and similar break-even points. Its primary gain catalyst is theta decay and minimal stock price movement. However, an important distinction is that the butterfly is vega negative when in the winning zone, meaning that declining IV will allow gains to grow at a quicker rate.

How does this affect your trade opening decision? When IV is lower, the likelihood of further decline is reduced, making a calendar spread a favorable choice since any rise in IV can benefit the trade. Conversely, when IV is elevated and a decline is more probable, a butterfly spread may be advantageous as any drop in IV can enhance the trade’s performance.

Spreads for Stock Price Movement in Any Direction

Finally, let’s examine common spreads designed for significant stock price movement, whether up or down. A long straddle or long strangle consists solely of long legs, making them always vega positive. Rising IV will mitigate the effects of negative theta, while falling IV will exacerbate the price decrease due to negative theta. This is why straddles and strangles are typically employed in the lead-up to earnings announcements, where a guaranteed IV increase can counteract some of the negative theta.

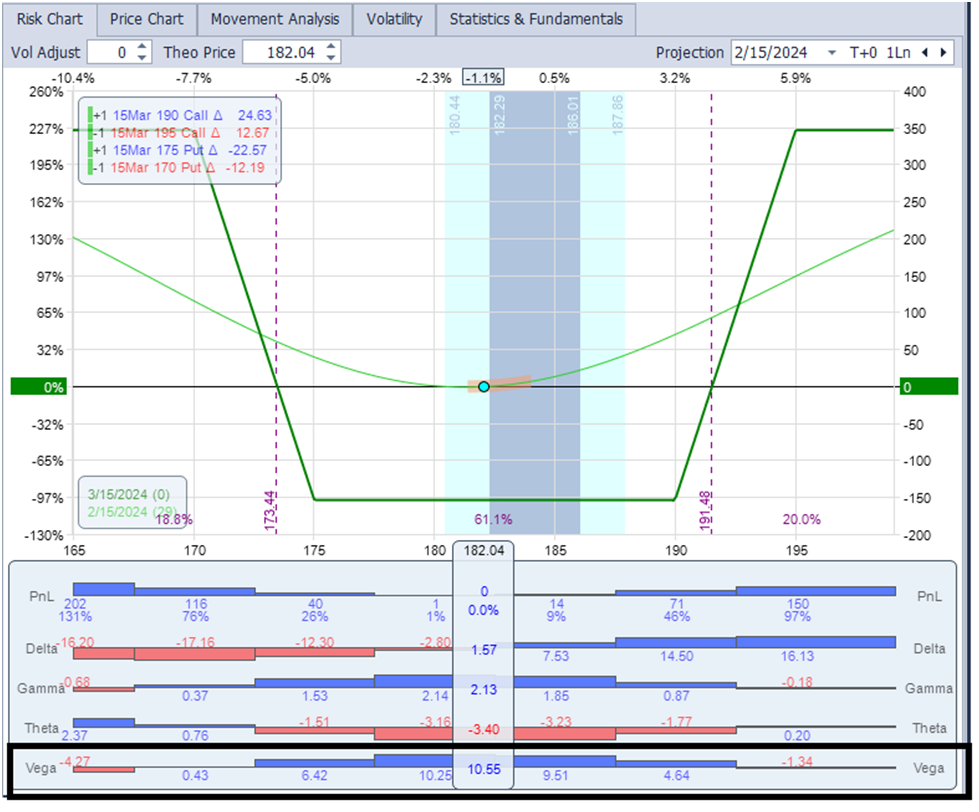

A reverse iron condor (RIC) is the opposite of the iron condor, consisting of an OTM call debit vertical spread and an OTM put debit vertical. The distance from ATM affects the risk-reward setup. The RIC is vega positive when in the losing zone between the put and call wings, meaning any decline in IV will accelerate losses. However, the trade becomes vega negative when the stock price moves into a winning zone, ensuring a profitable trade regardless of IV fluctuations.

While there are certainly more complex trade setups available for these scenarios, this article has covered some of the most popular strategies. You can see how current IV can significantly impact your decision on which trade setup to utilize.