The human mind often struggles to grasp the true power of compounding. Consider this scenario: you retired in 1985 with a nest egg of $100,000 and a home that was fully paid off.

At the end of 1985, you decided to invest that $100,000 in an S&P 500 mutual fund. You lived off dividends and Social Security, enjoying your retirement without financial stress. While you spent the dividends, you kept the portfolio invested, allowing it to grow.

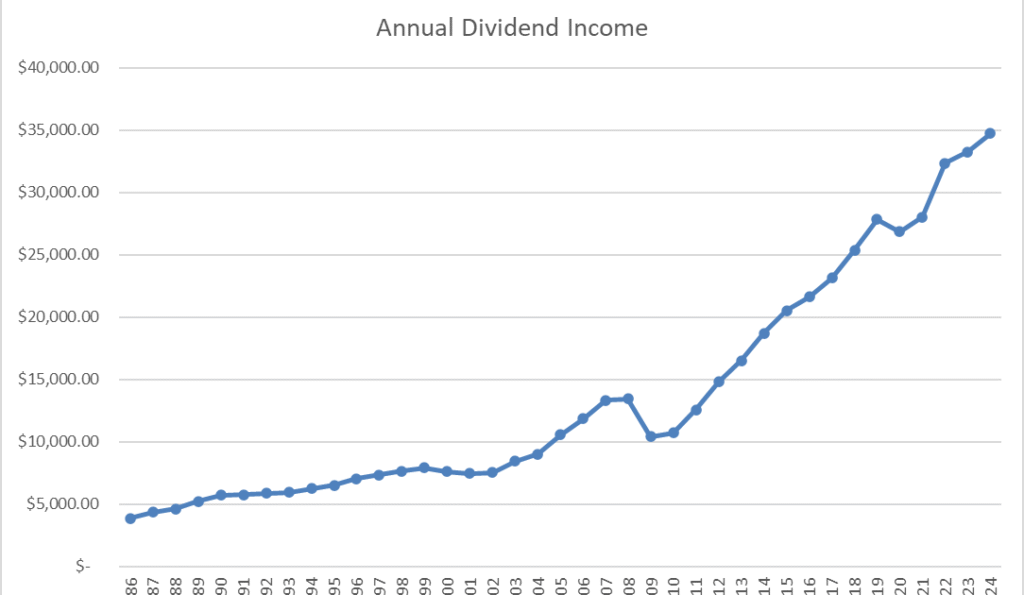

In your first year, you generated nearly $4,000 in annual dividend income. Fast forward to today, and you’re on track to generate over $37,000 in annual dividend income. Imagine the transformation!

By the time you pass away in 2025, your portfolio has grown to an impressive $3.2 million. Remarkably, 97% of that gain in net worth occurred during the last 40 years of your life. You lived fully, enjoying your retirement while watching your investments flourish.

If you had no heirs, you might be one of those individuals who make headlines for donating millions to charity. However, if you do have children or grandchildren, they would inherit a substantial amount, providing them with a financial cushion.

Interestingly, whenever I share this scenario, someone often comments that “they didn’t enjoy their money.” This perspective stems from a misunderstanding of compounding and the nature of long-term stock returns.

To clarify, some individuals see the final figure of $3.2 million and mistakenly believe that this wealth was always available. They assume that you should have spent more during retirement. However, that $3.2 million was not realized until the end of your journey.

If you had spent more when you first retired in 1985, you might have run out of money by the late 1980s or early 1990s, leaving you with nothing to show for it. The reality is that you enjoyed life, managed your schedule, lived in your paid-off home, and received Social Security checks alongside rising dividend income. Perhaps you even had a corporate pension, though many people today do not have that luxury.

This highlights a common misconception: for most people, having $1 million means spending $1 million. In contrast, smart investors understand that having $1 million equates to having a small army of dollar soldiers working tirelessly for you, providing income and financial freedom.

Ultimately, this thought exercise serves as a reminder of the power of compounding and the importance of long-term investment strategies. As I often say, “I frequently think about that.”