Few companies are as integral to daily business operations as this one. Payroll is a constant necessity—regardless of economic conditions, employees expect timely and accurate payments. This company has capitalized on this certainty, expanding its offerings beyond payroll into the broader human capital management (HCM) sector. With a substantial client base and a recurring revenue model, it has established itself as a cornerstone of dividend growth investing.

Global Payroll Powerhouse

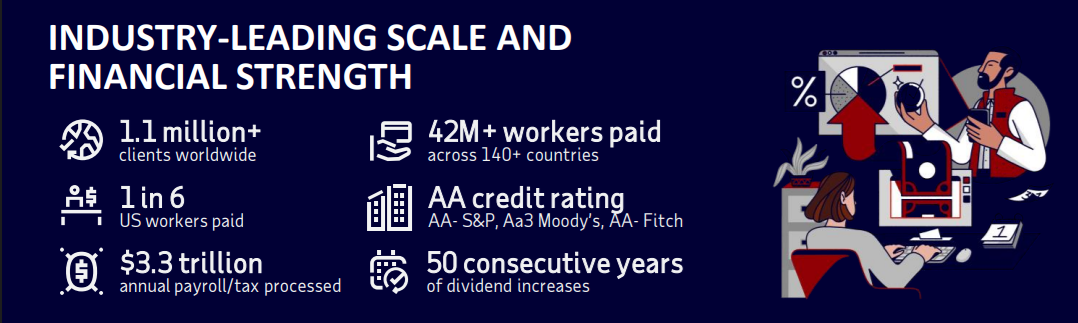

Automatic Data Processing (ADP) delivers cloud-based payroll and HCM solutions that integrate HR, benefits administration, time tracking, and compliance services. Operating in over 140 countries, ADP serves 1.1 million clients and processes payroll for 1 in 6 U.S. employees.

The company’s operations are divided into two primary segments:

-

Employer Services: This larger segment offers payroll, tax, HR outsourcing, workforce analytics, benefits administration, and compliance services. It generates steady, subscription-based revenue linked to employee counts and service breadth.

-

Professional Employer Organization (PEO): Operating under the ADP TotalSource brand, this segment provides outsourced HR solutions through a co-employment model. While more cyclical, it offers robust growth and cross-selling opportunities.

ADP’s combination of scale, reputation, and global compliance expertise enables it to maintain a leadership position in an industry where trust and accuracy are critical.

Bull Case: Wide Moat in Payroll and HR

ADP’s bullish outlook is anchored in its scale, reputation, and recurring revenue model. Once integrated, ADP becomes a vital partner for businesses, fostering sticky, high-retention client relationships.

Playbook

The company benefits from a subscription model tied to the number of employees processed, meaning growth in employment directly translates to increased revenue for ADP. Built-in service upgrades, add-ons, and inflation-adjusted price escalators provide additional growth opportunities. With client retention above 92%, ADP’s revenue base remains highly predictable.

Growth Vectors

-

Cross-Selling Services: Retirement planning, benefits administration, workforce analytics, and digital hiring tools enhance client relationships.

-

Technology Investments: The launch of ADP Lyric, its new AI-powered platform, modernizes the HR suite, positioning ADP against newer SaaS competitors.

-

Strategic Acquisitions: The recent acquisition of WorkForce Software enhances time tracking and scheduling solutions, a crucial area for employers.

-

Labor Market Tailwinds: With tight labor markets, payroll volume remains robust. ADP also earns interest income from client funds held before payroll distribution—an attractive feature in high-rate environments.

Economic Moat

ADP’s competitive advantage stems from high switching costs and regulatory expertise. Payroll errors can be costly, both financially and legally, making companies hesitant to switch from a trusted provider. ADP’s extensive compliance infrastructure across various jurisdictions further solidifies its advantage.

Bear Case: Cyclical Risks and Rising Competition

Despite its resilience, ADP faces certain risks. Its performance is closely tied to employment cycles, and competition is intensifying.

Business Vulnerabilities

In economic downturns, payroll volumes tend to decline, particularly among small- and mid-sized businesses. The PEO segment is particularly vulnerable, as small businesses may reduce staff or shut down entirely. Additionally, payroll services have become more commoditized, pressuring ADP to bundle services to justify premium pricing.

Industry & Market Threats

-

Macroeconomic Slowdowns: Layoffs and slower hiring directly impact payroll volume.

-

Pricing Pressure: Cloud-native SaaS competitors offer more affordable and agile products for mid-market clients.

-

Execution Risks: Integrating acquisitions and launching new platforms like Lyric present operational challenges.

Competitive Landscape

ADP competes with Paychex, Paylocity, Workday, and SAP, among others. While ADP maintains unmatched global reach, competitors often excel in niche markets such as SMB payroll (Paychex) or enterprise HCM (Workday). ADP’s challenge lies in remaining technologically competitive while leveraging its scale and reputation.

Get the Dividend Income for Life Guide

Interested in retiring on dividends? The Dividend Income for Life Guide provides a roadmap for building sustainable income for decades—with clear steps, example portfolios, and smart strategies to follow. Whether you’re nearing retirement or just starting out, this guide helps you structure your finances around income rather than speculation.

Download your free copy now »

What’s New: A Strong 2025

On August 8, 2025, ADP reported another impressive quarter:

-

Revenue increased by 7.5%, and EPS rose by 8%, exceeding analyst expectations.

-

Employer Services revenue grew by 8%, with 6% organic growth.

-

PEO Services revenue rose by 7%, with worksite employees increasing by 3% to 761,000.

-

Client retention stands at 92.1%, highlighting the stickiness of the model.

-

Interest income increased by 11% to $308M, reflecting higher rates.

-

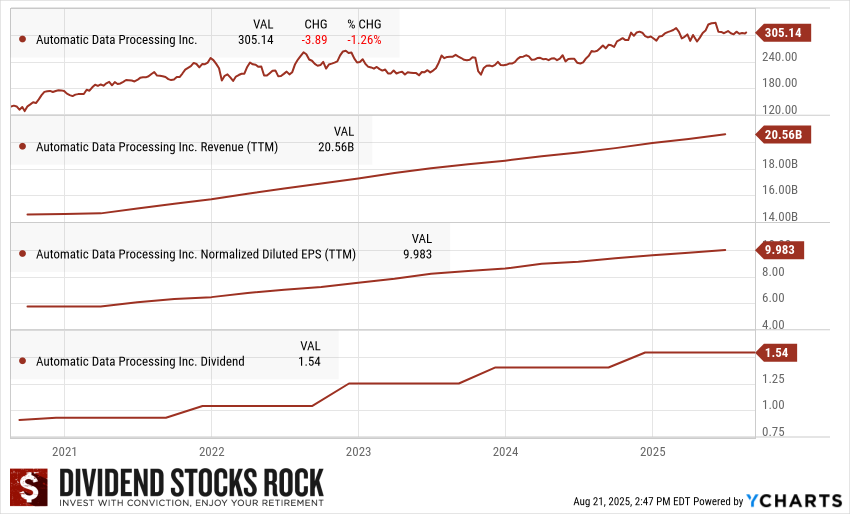

Full-year revenue reached $20.56B (+7%, +7% organic).

Looking ahead, ADP anticipates 5–6% revenue growth in FY26, 50–70 bps margin expansion, and 8–10% EPS growth.

The Dividend Triangle in Action: Consistent Climb

ADP’s Dividend Triangle showcases its long-term strength:

-

Revenue has steadily grown, reaching $20.6B.

-

EPS is just under $10, compounding at a healthy rate.

-

Dividends continue their reliable ascent, now at $1.54 per share. ADP is also part of the Dividend Kings list, boasting 50 consecutive years of dividend increases.

While ADP’s yield may not be high, its consistent double-digit dividend growth has compounded returns for decades. It exemplifies quality over yield—one of the most reliable income growers in the market.

Final Thoughts: The Payroll Giant that Never Sleeps

ADP combines a wide moat, resilient recurring revenue, and strong free cash flow generation. Its entrenched position in payroll and HR, along with technology upgrades and cross-selling potential, supports ongoing earnings and dividend growth. While cyclical risks and rising competition warrant attention, ADP remains a best-in-class dividend growth stock for investors seeking steady compounding over the long term.